Thank you to Dan Smith and Mike Ippolito for valuable input, review, and related discussions. The views expressed in this post are solely my own, and do not necessarily reflect those of the reviewers. You can also listen to our podcast covering this post on Spotify or YouTube.

Introduction

The debates around protocol financials are never-ending. Is Solana unsustainable because of its high inflation? Are Ethereum and Solana unprofitable to the tune of billions of dollars per year? Is it hopium to think that our tokens can be money? Do L2s have better economics than L1s?

This post builds on top of ETH Is Not Ultrasound Money, which I wrote over a year ago to explain some basic L1 economics. It’s time for an updated and more generalizable analysis.

If you’re looking for a single metric that tells you, “will the token price go up?”, unfortunately no such number exists. However, as in traditional finance, we can create standardized metrics that are actually useful. Today, the popular crypto financial analysis tools don’t even agree on key metrics, providing inconsistent definitions and measures across platforms. We can start by purging illogical (yet popular) metrics like network profit = fees – issuance or profit = burn – issuance. Then, we’ll make better ones, such as:

- Network TEV (Total Economic Value) = Network Fees + MEV Tips + Issuance

- Network REV (Real Economic Value) = Network Fees + MEV Tips

- Token Holders’ Net Income = REV – Operator Payments

This post focuses on blockchains’ native cryptoassets (e.g., BTC, ETH, and SOL). In particular, we will focus on measuring their ability to capture value by generating real income. At the end, we will discuss token value capture via other mechanisms (e.g., utility value and monetary premium).

Crypto vs. TradFi Metrics

Networks Are Not Companies

Before we can define any metrics, we need to pick our reference point.

For example, Apple Inc. is a discrete entity with attributable financials. It is legally structured as a corporation owned by its equity shareholders. We can assess the profitability of Apple Inc. The company earns income (e.g., sales for iPhones), pays expenses (e.g., paying employees), and retains profits.

However, cryptonetworks are not companies. Protocols like Bitcoin are simply a given set of rules, implemented in code, run permissionlessly by independent operators. They are distributed networks, not discrete entities. They are generally viewed as not qualifying as a common enterprise. Most major chains’ native assets (e.g., BTC, ETH, SOL) have no governance rights over their respective networks.

These networks neither make nor lose money, they simply exist. Financial terms such as “income” and “expense” are definitionally relative to some clear reference point (e.g., your income is someone else’s expense), but no such relevant entity exists here. An abstract notion of “network profit” here is as sensible as asking what the internet’s profitability is.

Tokenholder Income

So what is the correct reference point here when people try to assess “Ethereum profit”? Are we just talking about un-staked ETH holders? Just ETH stakers? Or maybe all participants in the Ethereum network (e.g., ETH holders, validators, other infrastructure providers, etc.)?

These all yield different results. For example, if your reference point is only un-staked ETH holders, then issuance is purely an expense. But if your reference point is only staked ETH holders, then issuance is both income and an expense.

This post mostly focuses on calculating financial metrics such as net income across all token holders in aggregate. This is the most broadly useful way to analyze tokens’ ability to generate income, understand networks’ financial health, and compare them vs. peers. For example, if you wanted to value a token by placing a multiple on its ability to generate income (analogous to P/E valuations), then the net income of all token holders is the applicable metric. You can calculate and compare this number for BTC vs. ETH vs. SOL apples-to-apples.

That’s not to say that financial metrics for subsets of holders (e.g., net income for just token stakers) are not valuable. They can also be valuable, and are indeed necessary for any economically rational individual holder to assess as well. If you’re opting to stake, you especially want to know the income statement of being a staker in addition to the overall income statement for token holders. Both can impact your valuation analysis. More on this later.

I’ll also note that you may find these token-centric financial metrics to be more useful for PoS assets (e.g., ETH and SOL) than PoW assets (e.g., BTC). PoW assets tend to be more commodity-like relative to PoS assets which tend to be more equity-like. So at times, these PoW metrics will seem a bit silly in the way that calculating the income of holding gold would seem silly. Nobody buys gold or BTC looking for the most productive income-generating asset. Nonetheless, it’s helpful to include both PoS and PoW examples throughout to highlight these differences and deepen our intuitions around them.

Taxes

Some of the most prevalent misguided arguments here concern the relation between real-world taxes, profitability, and network valuations. So, let’s get the boring tax stuff out of the way first.

Believers that staking issuance is a “cost to the network” often cite that issuance causes “sell pressure” due to stakers paying taxes. Depending on a given staker’s jurisdiction, staking rewards may be treated as taxable income. Reducing issuance rewards and/or burning user payments would preclude this. This is analogous to a company conducting share buybacks vs. paying a dividend. Holding market cap constant, shrinking the outstanding supply increases the per-share asset price. This gives the asset holder optionality to decide when to create a taxable event upon sale, and potentially receive a lower tax rate (depending on local capital gains tax treatment).

When these taxes on staking are present, they are comparable to an individual equity holder paying taxes on their dividend income. Importantly, dividend taxes are not expenses to the respective company, and they do not reduce its earnings. Whether or not a company’s individual equity holders decide to live in jurisdictions where dividends are taxed is separate from the company’s financial metrics, and thus its inherent value. Investors are free to live in jurisdictions where they will not be taxed.

This is very different from corporate taxes which do reduce a company’s net income. However, there is no comparable notion here in cryptonetworks. There is no corporate tax rate applied to “Bitcoin’s income”, as no such relevant entity exists. To be clear, this isn’t something magical about tokenization or being onchain that makes Bitcoin exempt from corporate taxes. You can’t just slap a token on a company and call it decentralized.

Imagine a company (e.g., Coinbase) that operates a network and earns income doing so. Say they even put all of their company operations onchain. Users pay fees directly into an onchain treasury, and the company could pay expenses (e.g., employee salaries) out of it. Obviously putting the assets onchain didn’t just exempt the company from its obligation to pay corporate taxes. It’s a company.

Rather, the distinction comes down to the details of the network in question. For decentralized networks such as Bitcoin, these concepts clearly do not map over. It lacks the hallmark characteristics for entity treatment for federal tax purposes: two or more parties who jointly conduct and share the profits from an activity that constitutes a business. Rather, we have many permissionless parties operating independently in a decentralized manner.

So as funny as it may sound, it should be clear now that issuance to stakers is not a “cost to the network”, even if it has potential associated “sell pressure.” Look, none of this is to say that inflation doesn’t matter. It does! That’s all the more reason why we need to start explaining it logically. Stop saying that inflation is a cost to the protocol.

Issuance rewards can influence the behavior of network participants, and they may even impact the token price in practice. But this inflation matters in much the same way that it matters if a company decides to conduct a share buyback or pay out dividends. They don’t change the company’s bottom line, but it can still make sense to cater to different potential investor bases that may prefer a certain method of capital distribution for tax efficiency.

I have long argued that tax inefficiency is one of the stronger arguments for why to avoid high token issuance. You’re potentially forcing some subset of holders (stakers) to recognize taxable income even though no real value is generated or returned here. This is unlike traditional corporate dividends which are returning real profits to equity holders (similar to paying out network fees to stakers).

Imagine that you own 100% of the tokens for a PoS network, and it issues 100% of new tokens to stakers. This makes it clear why it seems silly to tax this issuance. This looks like a stock split – it’s just a redenomination. Another potentially logical tax treatment would be to give an equivalent tax deduction for all token holders (both stakers and non-stakers) as they all bear the offsetting issuance expense. Unfortunately, we don’t yet have this level of nuance in most crypto tax law today. So we can complain all we want that crypto staking tax laws are silly, but that’s the reality at the moment. Given that many investors live in areas where staking rewards are tax inefficient, this may impact their willingness to purchase that asset.

In an efficient market this should not impact the asset’s valuation. Investors could shield this income by operating in a jurisdiction which does not tax it, or it is possible that technical solutions like non-rebasing LSTs can be used. They can realize the asset’s full value. Let’s consider some examples:

- Example 1 – We all agree that a token is worth $1bn based on the potential income from earning it. However, they have some weird really high issuance, and you live in a place where that would create a huge tax burden. You probably won’t buy the token, but someone living in a jurisdiction that doesn’t tax their issuance rewards should be willing to pay the $1bn. Alternatively, it is possible that converting the token into a non-rebasing LST addresses this concern.

- Example 2 – Imagine that I would beat up any of my neighbors who hold ETH, and take 40% of it from them every year. Did I just make ETH as an asset fundamentally 40% less valuable? No, of course not, you should just move away from being my neighbor. The government is kinda like that here. In an open market, what matters to the asset’s fundamental value is what is inherent to the asset and what rights are available to any holders.

Again, in practice there are obviously large buyer bases you want to appeal to who may live in jurisdictions where high staking rewards are tax inefficient. Staking tax laws are unclear in many jurisdictions still, but the conservative treatment in many large countries is currently to just pay taxes on the rewards received as income. Potential investors will assess their own income for holding the asset based on their own jurisdiction, and taxes impact this. Additionally, you may not want to create incentives for token holders to feel forced into using (non-rebasing) LSTs. That may be reasonable, but we need to account for these implications properly, and that requires defining the issue properly to begin with.

Crypto Financial Metrics

Proof-of-Work vs. Proof-of-Stake

We tend to see the following split between PoW vs. PoS tokens:

Total Economic Value (TEV)

While certain relative terms like profitability don’t apply at a network level, we can still of course calculate other useful network-level statistics. Now, we will start to standardize some financial metrics which can be used across any cryptonetwork.

Network TEV (Total Economic Value) is defined as follows:

TEV = Network Fees + MEV Tips + Issuance

We count equally here all network fees and other forms of MEV tips paid by users regardless of the type of payment (e.g., base fee vs. priority fee vs. direct transfer to staker), or the ultimate use of funds (e.g., burning vs. transfer to a staker). Also priority fees are MEV anyway.

What matters is that these are base network-level value flows. For example, TEV does not include app-layer fees (e.g., Uniswap UI fees). Similarly, TEV does not include MEV profits captured by arbitrageurs which are not paid along to stakers.

TEV is useful in setting the stage for our metrics below. It gives us the topline amount of base layer value in a given time period to be allocated amongst token holders and network operators. As we noted above:

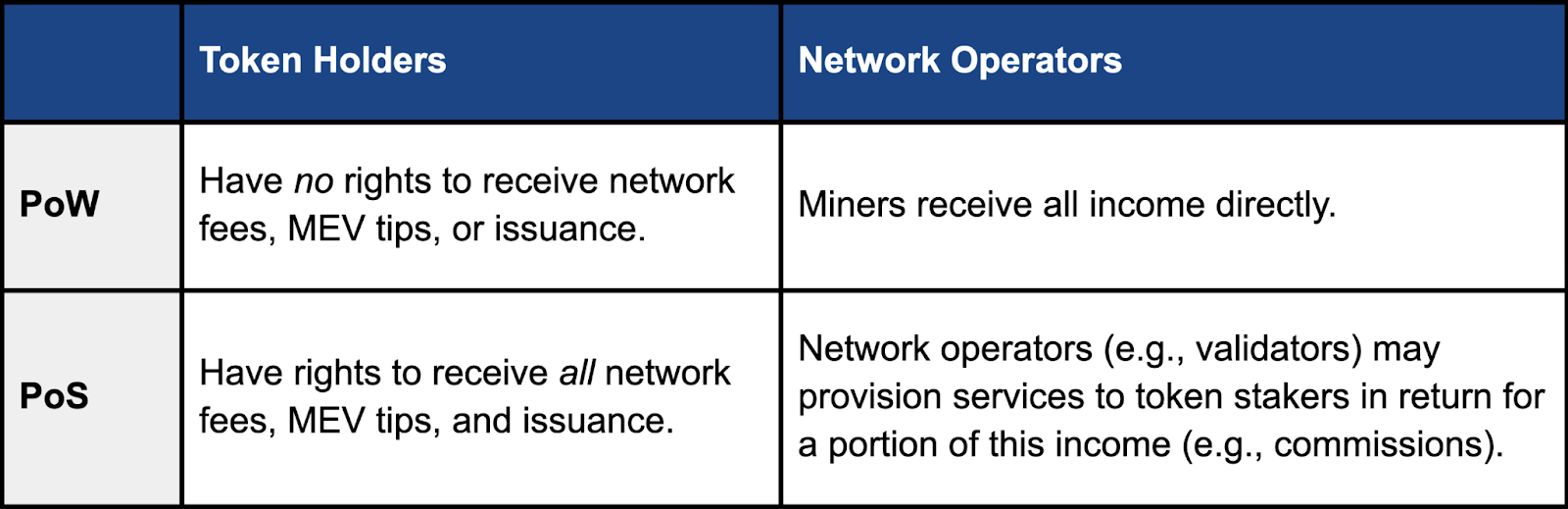

- PoS – Token holders have rights to receive all TEV. They typically keep most TEV, while paying out some portion to network operators (e.g., validator delegates) as a commission.

- PoW – Network operators (e.g., miners) have rights to receive all TEV. This is economically equivalent to PoS with 100% commissions.

Given this, we could say the total income (i.e., revenue) of all traditional PoS token holders = TEV. They are productive income-generating assets. Conversely, the total income of all PoW token holders = 0. For example, BTC holders have no rights to receive any TEV. BTC’s value proposition is as a monetary asset, not an income-generating asset.

Real Economic Value (REV)

Next, we will strip out inflation, giving us network REV (Real Economic Value):

REV = Network Fees + MEV Tips

REV excludes issuance, as that is not real value generated. A couple of terminology notes:

- Our relevant inflation metric here is inflation of the token supply. This differs from some popular traditional finance metrics, such as real yield = nominal yield – inflation rate, where the relevant inflation metric is often the change in purchasing power of the currency against some basket of goods (e.g., using CPI rather than inflation of the US dollar supply).

- Blockworks Research has recently used “TEV” to mean what we redefine as REV here (i.e., all network fees and MEV). In tandem with this post, Blockworks Research has adopted this new terminology of TEV and REV respectively.

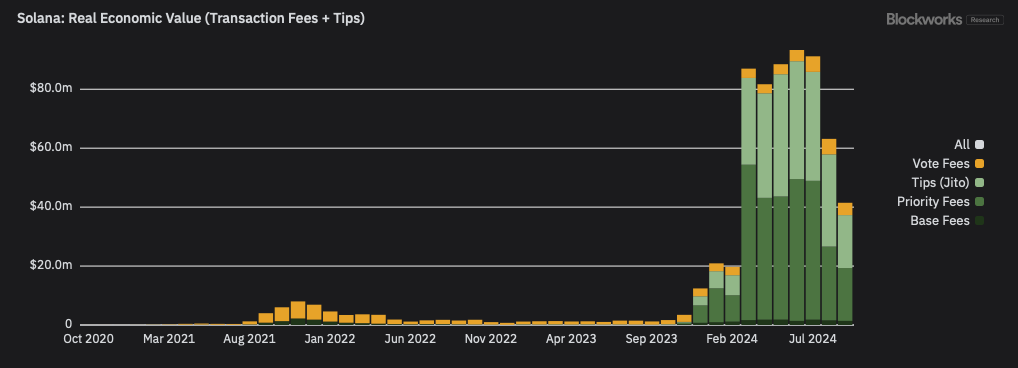

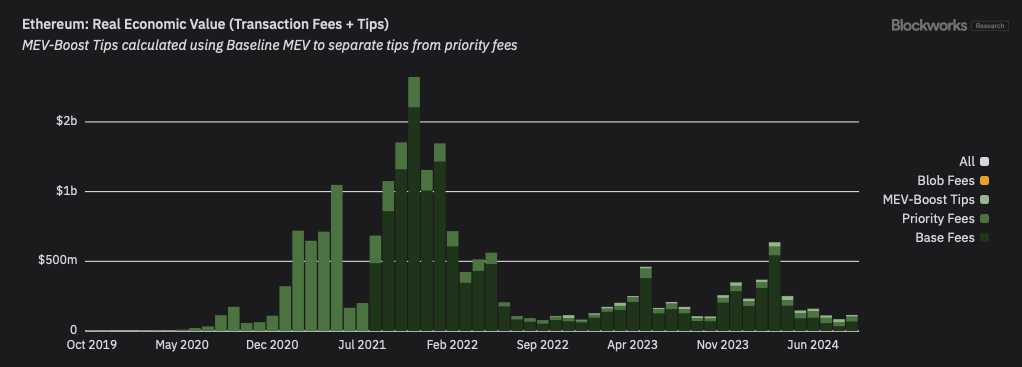

Monthly REV for Ethereum and Solana is shown below:

We see that both Solana and Ethereum have been running at a pace of ~$1bn REV annualized lately. Looking a bit further back, Ethereum put up some monster numbers from 2021-22, frequently surpassing $1bn REV per month.

REV is often the best single metric in assessing real demand to use a given network. Common user-centric metrics used in Web2 (e.g., DAUs) are trivially sybilled in crypto (please stop using active addresses as = active users!), but money talks. REV is generally non-gameable. It’s not a surprise that the charts above have some meaningful overlap with their respective token price charts.

Token Holders’ Net Income

Now we’ll turn to where that value goes. Who does TEV and REV end up accruing to? We especially want to measure what value the token captures (or loses).

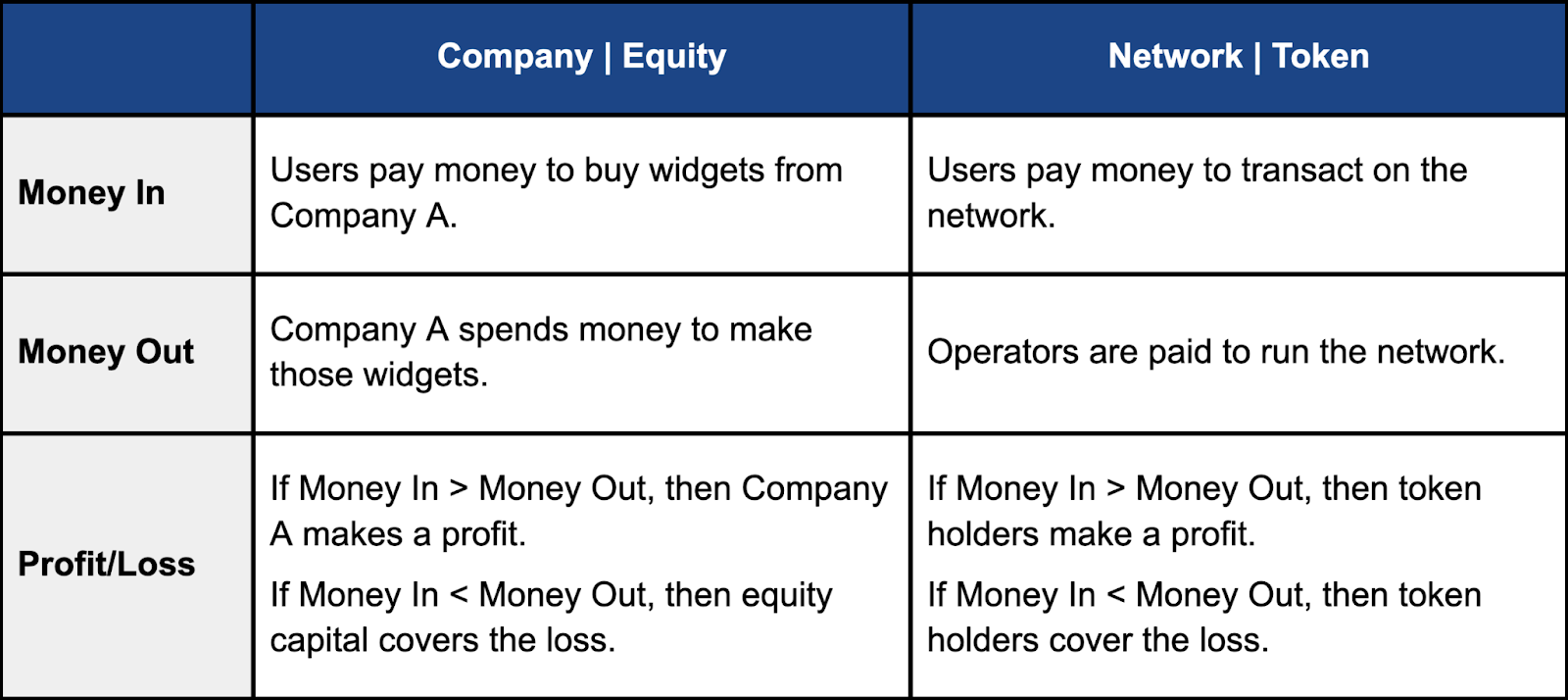

First, let’s consider some oversimplified points shared by companies, networks, and their respective assets:

Note the more abstract use of “money in” and “money out” terminology here, as opposed to “income” or “expense”. For a company, these terms do indeed map to each other (i.e., money in = income, and money out = expense). But once again, networks are not companies. Even though we will assess profitability from the token’s perspective, the meaning of “income” and “expense” differs across different types of token holders (e.g., REV is income to PoS token holders, but not to PoW token holders). More on this later.

Focusing on the network setting, it should be clear that “Money In” = REV. From the token’s perspective, “Money Out” is whatever portion of TEV is paid to core network operators (e.g., miners receiving fees and block rewards) other than token holders. If operator payments > REV, then token holders necessarily cover the shortfall via inflation subsidies.

This leaves us very simply with the following net income (i.e., profit) for all token holders:

Token Holders’ Net Income = REV – Operator Payments

Where:

Operator Payments = Portion of TEV paid out to network participants other than token holders

These “operators” typically consist of the core infrastructure providers that produce blocks and confirm them in consensus. They bear real-world (offchain) costs in operating the network (e.g., hire employees, buy hardware, pay ongoing energy costs, etc.). They are reimbursed (+/- some profit) by receiving some portion of TEV. From the token’s perspective, these operators include all other essential network participants who have rights to receive some of the TEV produced:

- PoW Miners – Whoever mines the block is entitled to receive all TEV in it.

- PoS Validator Delegates – While token holders have rights to receive all TEV in a block, there still exist real-world costs associated with operating the network. Typically, token stakers will enter into agreements with other parties to operate the necessary infrastructure in exchange for some portion of the TEV. Stakers typically delegate to a centralized staking-as-a-service operator (e.g., Coinbase) or a decentralized liquid staking protocol (e.g., Lido) that consists of many operators. Alternatively, they could pay to run their own infrastructure.

- MEV Infrastructure – Similarly, miners and validators may further offload some of their duties to other supply chain operators in exchange for a portion of TEV. For example, Jito Labs takes a 5% commission on all user payments sent through its MEV auction en route to validators.

- Other – The above encompasses all Operator Payments in traditional networks (e.g., Bitcoin, Ethereum, Solana). However, in less traditional cases, note that there may exist any other arbitrary value leakage away from tokens. For example, a chain may programmatically send a portion of all new block rewards to an address controlled by the centralized team who created the protocol code. Alternatively, the protocol may issue new tokens to application developers building on the network. We will consider any of these arbitrary uses as “Operator Payments” for our purposes here, as they are all equivalent real losses to token holders. They are non-cash expenses, analogous to stock-based compensation in traditional finance.

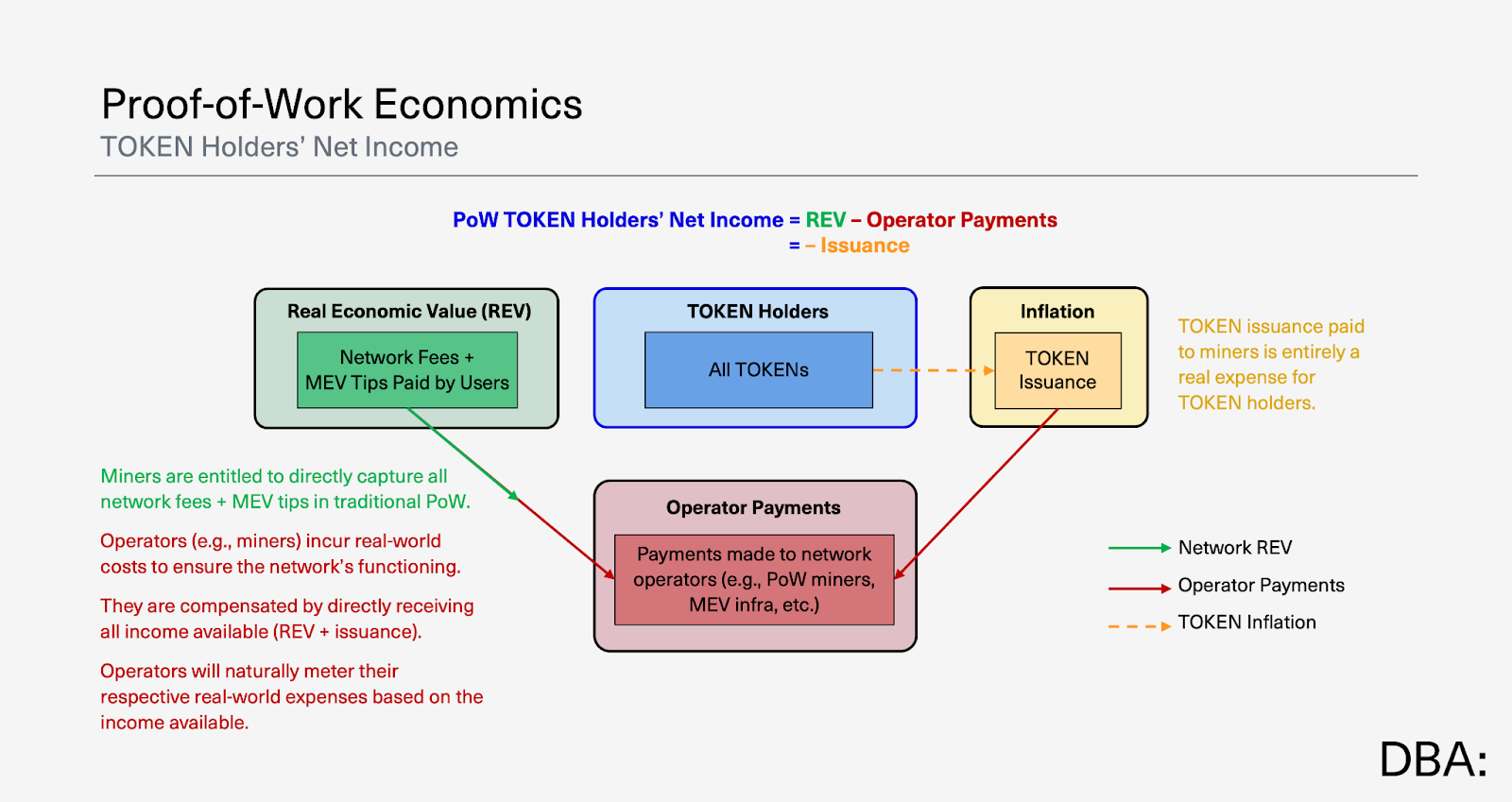

Proof-of-Work

Now, let’s see the difference between PoS vs. PoW. For traditional PoW, where 100% of TEV goes to the miners, we have Operator Payments = TEV. TEV = REV + Issuance, so we can simplify our equation from above to the following:

PoW Token Holders’ Net Income = – Issuance

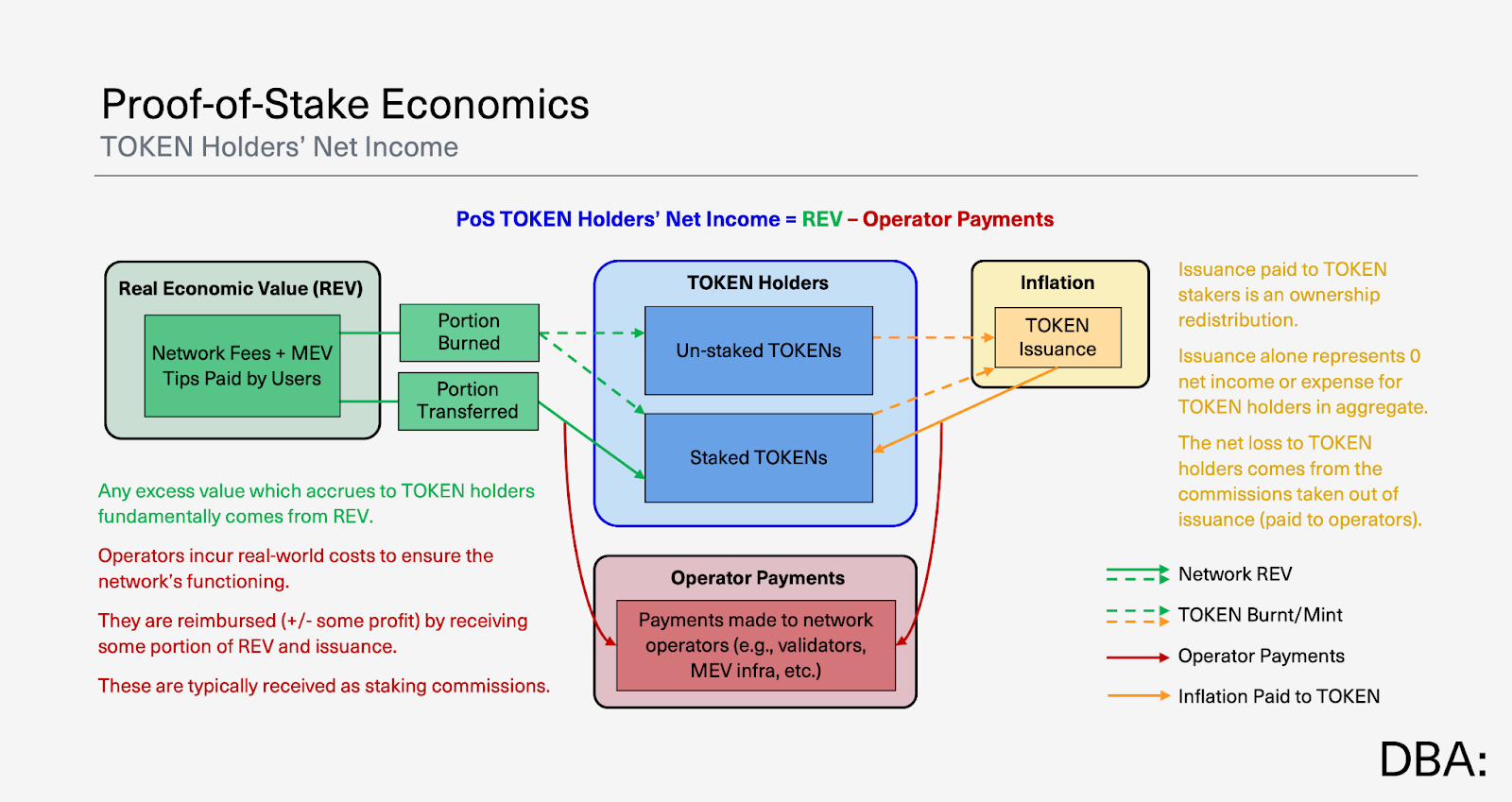

Proof-of-Stake

Traditional PoS token holders are by default entitled to receive all TEV, so they must in turn negotiate economic terms (i.e., commissions) with operators (or run their own operations). Token holders keep the excess value generated (or subsidize the loss). The picture is slightly more complicated here as a result:

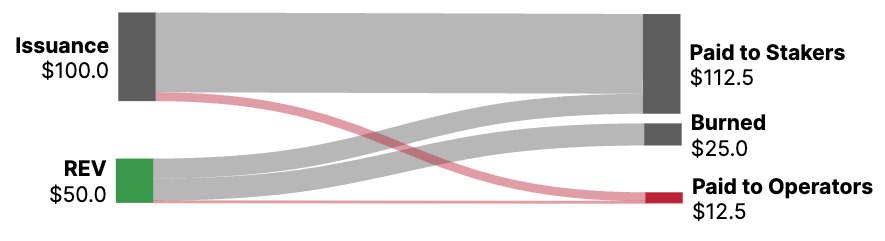

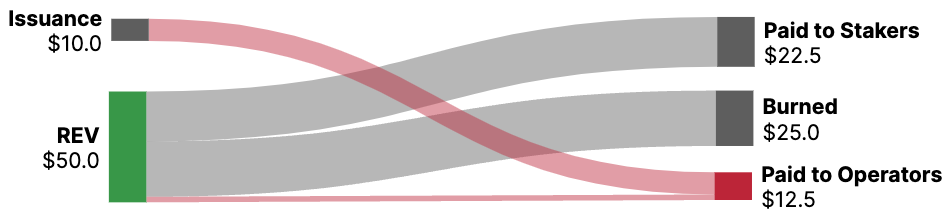

Let’s consider a simplified example. For a given time period:

- Issuance = $100 worth of tokens

- REV = $50 worth of tokens, of which 50% ($25) is burned, and 50% ($25) is to be paid to stakers.

- Operators charge a 10% commission on all issuance ($10) and REV paid ($2.5).

We can calculate:

PoS Token Net Income = REV – Operator Payments = $50 – $12.5 = $37.5

To see the role of inflation, let’s consider another example where we make a couple changes:

- Issuance = $10 worth of tokens

- Operators charge a 100% commission on issuance

- Everything else remains the same

We’re basically just removing the $90 being issued and sent to stakers:

Token holders’ net income is unchanged:

PoS Token Net Income = REV – Operator Payments = $50 – $12.5 = $37.5 tokens

We reduced inflation, but the token holders’ profit is unchanged. The only difference is that there is directionally less incentive to stake rather than hold idly (because the staking yield is reduced). On its own, PoS issuance is simply an internal tax which redistributes network ownership among token holder subsets to incentivize staking.

When people argue that “issuance is a cost” in PoS networks, it’s usually a fuzzy attempt to get at “isn’t inflation bad for token value capture somehow? It seems like it should be bad, right?” However, the only real expense to token holders in aggregate is the payment made to operators. This is usually seen in staking commissions in PoS vs. PoW which can effectively be viewed as 100% commissions.

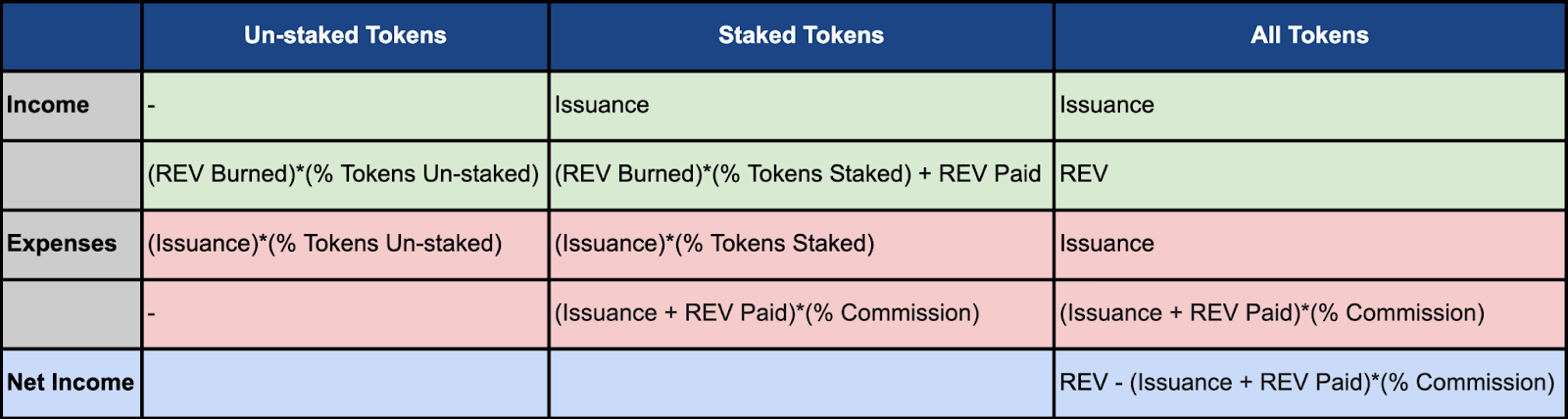

Net Income = Income – Expenses

As noted earlier, we did not use the traditional basic formula for net income = income – expenses. We spoke of generic network concepts of “money in” vs. “money out” then proceeded to calculate token holders’ net income = REV – operator payments. It always works out that way, and these metrics are directly comparable across networks.

However, you can of course calculate token holders’ net income as income – expenses. The reason I opted not to do so earlier is because it gets messy. In particular, what’s considered “income” vs. an “expense” varies based on what we’re evaluating. For example, REV is not income to BTC holders, but it is income to ETH holders. As a result, any attempt at defining “income” would not be directly comparable across the two.

Now, it is still incredibly useful to calculate net income = income – expenses when evaluating any subset of token holders (and you’re not concerned with directly comparing the line items from PoW vs. PoS). For example, if you are considering staking a given token, you especially need to also know the expected net income from staking. The inverse is true if you’re considering holding and not staking that token.

In both cases though, you also need to care about the net income of all token holders in aggregate. That is the measure of the token’s overall value capture from generating income, and hence is a major component in its valuation. Imagine a network with high issuance and low staking participation. The income statement for stakers might look great. But if you ignore the fact that this chain has 0 REV because it has no users, and it’s expensive to run all the boxes, you’re probably going to end up being disappointed with the token price over time nuking your returns. This is captured in the joint income statement of all token holders. You also need to assess the expected stake rate over time. If you made your staking income projections based on a low stake rate, but then a bunch of other token holders go stake, this would impact you.

So, all three subset income statements are necessary here in PoS. You will also notice that in aggregate they net out to our formula from before:

Token Holders’ Net Income = REV – Operator Payments

Payments to Operators

We have established that running a decentralized network requires some real-world costs. Operators are then reimbursed (+/- some profit) by receiving some portion of TEV.

This will be the trickiest part to calculate because, unlike a company, we don’t have a shared entity with pooled costs. We have many independent operators each with their own expenses. They are also paid independently by completely independent users, token holders, and other operators. We need to stitch all of these numbers together to try to make our calculation here.

In PoW, this isn’t too complex. Miners directly receive all TEV, of which issaunce is a real non-cash expense to token holders, similar to stock-based compensation in traditional finance. Miners are incentivized to expend an amount of energy (and money) which is roughly equivalent to the TEV available.

In PoS, token holders play a more central role in these value flows. By default, token holders are entitled to receive all TEV. So ultimately, these token holders should be expected to pay for the provisioning of these services that are required to run the network. These payments are usually plainly visible, but sometimes they’re a bit harder to track:

- Onchain – Most expenses are clearly visible onchain in the form of commissions. This typically includes centralized staking-as-a-service operators whom stakers delegate to (e.g., Coinbase), liquid staking providers (e.g., Lido) whom stakers delegate to, and MEV infrastructure providers (e.g., Jito Labs) who run MEV auctions. These parties each tend to take 5-10% commissions on their relevant payment streams.

- Offchain – Offchain economic arrangements may also exist to pay for network operations, in which case the costs may be less clear.

As an example of the latter, consider a large staker operating their own validators (rather than delegating stake). Much like a delegated operator, this holder does still incur a real cost of running validator infrastructure (e.g., they hire an internal team to manage nodes). These are relevant costs from the token’s perspective. In assessing their own profitability, this individual staker would subtract whatever they spend on maintaining the requisite infrastructure out from their 100% rewards. These offchain economics are why calculating operator payments can be tricky to reason about.

Sometimes even the onchain data can be a bit misleading. This is because those large stakers who run their own validators are often registered onchain as 100% commission validators. A simple analysis of the onchain data here would overstate the amount being paid for operations. However, in reality this token holder is just keeping all of the rewards. Because they are their own operator, they pay the real-world expenses themselves. That is what flows through to their bottom line.

So here is where we end up on operator payments in PoS networks:

- Most costs are very clear and can be accounted for as such. This includes commissions taken by delegated validators (e.g., Coinbase), liquid staking DAOs (e.g., Lido), and MEV infrastructure providers (e.g., Jito Labs).

- Some costs are unclear, in which case I think there are different approaches which can be reasonable in different circumstances.

The main point to work around is that 100% commission to self-stakers. Let’s consider the range of options:

- Count as 100% operator payments – This wouldn’t make much sense. Treating this like a typical 5% commission taken by delegates would completely skew the calculation away from reality. It would overestimate what’s being spent for operator expenses (i.e., paying to run the nodes) vs. accruing to the token as profit.

- Count as 0% operator payments – It’s clean and easy to carve these out and count them as having 0 cost. This is at least much closer to reality, but still not quite perfect.

- Estimate operator payments – For the most accurate picture, you can try to estimate the real expenses borne by operators.

For estimation, you may simply apply the average commission of typical validator delegates. For example, if all typical Solana validator delegates charge a 5% commission on average, then maybe we just assume that all 100%-commission validators actually spend 5% on real operating expenses. There are plenty of other different ways to calculate this average payment, but you get the idea.

Alternatively, you could also try to calculate the estimated real-world input costs of a validator (e.g., estimating server costs and employee time).

Expenses Paid by Operators

Calculating the estimated real-world input costs of running network operations is an incredibly valuable calculation to conduct in any case. It will allow token holders to understand if they are underpaying or overpaying infrastructure providers.

These real-world expenses paid by operators generally differ from the payments made to operators used earlier in calculating the net income to token holders. The difference between them is the operators’ profit or loss. For example, the commissions paid to staking-as-a-service companies may be way higher (or lower) than what they actually spend on running the infrastructure, leaving them with a big profit (or loss).

The number used earlier in calculating token holders’ bottom line profitability is what they actually paid those operators. As a simple analogy, imagine the following:

- Company A sells widgets to consumers, and they generate $1mm in annual revenue doing so.

- Company A’s only OpEx is paying $1mm to Company B who manufactures the widgets.

- Company B is deeply unprofitable. It costs them much more than $1mm to manufacture the widgets.

This could be concerning if you’re a shareholder of Company A. Maybe Company B will go out of business. Then Company A’s only option would be to find another widget manufacturer that sells them for more than $1mm. Company A would be unprofitable if they can only resell them to consumers for $1mm. However, at least for today, Company A’s net profit is of course 0.

The same logic holds in accounting for operator payments from a token holder’s perspective. Even if the network’s operators are being subsidized in some external way, the payment from a token holder’s perspective is only that which they pay today. It’s important to understand these subsidies though, because they may indeed be unsustainable. For example, in the extreme, imagine a foundation directly running all of the network’s thousands of validators at a loss. Alternatively, subsidizing these operations may be perfectly sustainable in other cases, such as if running validators acts as a loss-leader for another profitable business line.

As mentioned, we also want to understand these operators’ real-world expenses for the opposite reason. What if it looks like the operator payments paid to them in commissions far outweigh what it should cost to operate them? Token holders may want to then look to see how they can reduce payments to operators and increase their own profit.

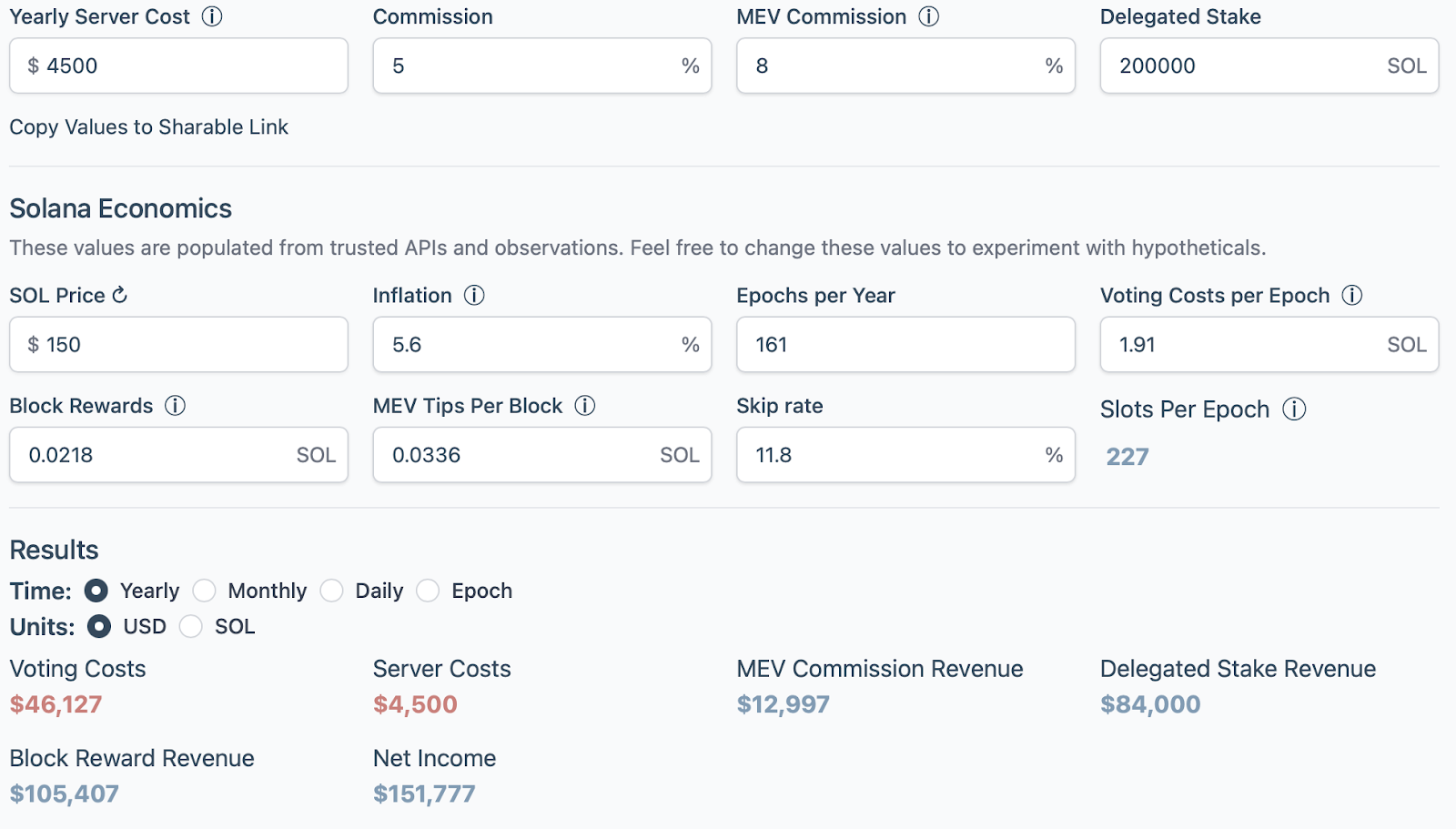

Let’s look at Solana validator economics here as an example just to get some order of magnitude ideas. Solana is more expensive for validators to run compared to most networks. The resource requirements are higher than average, but it’s certainly not as unattainable as is commonly believed. You can run a Solana validator full node for as low as $350/month. Average Solana validator server costs range from $350-700 per month. Let’s just take $500/month x 12 months x 1,400 validators = $8.4mm p.a. for all validators.

Note that running validators also carries very meaningful associated labor costs. These can be very difficult to estimate given their wide dispersion (e.g., solo staker vs. part of a large staking company running many chains), so we won’t pick a uniform number in this post. You can play with different assumptions. In general though, these can be expected to be higher than server costs.

Additionally, validators must cover voting fees. This is by far the biggest contributor to Solana validator costs. This is rather unique to Solana in that all votes are normal onchain transactions. They pay the 0.000005 SOL base fee for each slot, which translates to a bit under 1 SOL in voting fees paid per day for each validator. With SOL trading around $150 currently, we have $46k per validator p.a. x 1,400 validators = $64.4mm p.a. spent by all validators on vote fees. Note that while this increases operator expenses (which they would presumably want to be repaid for), it also equivalently increases token holders’ income as well.

You can play with this Solana validator calculator to run different assumptions:

Because of the high costs associated with running a Solana validator, you need quite a bit of stake to breakeven (either your own stake or delegated). The SFDP (Solana Foundation Delegation Program) exists to help get validators started and promote a healthy set of operators. This is done primarily with stake matching (up to 100k SOL) and helping to cover vote costs (at a reducing rate over one year) for smaller and newer validators.

Valuation Example

With all the basics in place, let’s put it together with a simple valuation example. Consider the price at which a single rational value investor would be willing to purchase all tokens for a given network:

- For simplicity, we will assume all REV for this network are paid in assets other than the native token (e.g., paid in USDC). This makes it possible for the investor to purchase all tokens, and allows us to isolate any effects of the token’s potential utility value as a currency. We’re just concerned about cash flows here.

- Whether or not there is any token issuance for staking rewards is of no consequence to the investor. It would simply be a token redenomination and redistribution to themselves.

- REV = $1bn. The investor would receive all REV.

- Operator payments = $100mm. The investor must then pay for the required operations of the network (e.g., validator nodes and MEV infrastructure).

- Investor’s net income = $1bn REV – $100mm operator payments = $900mm

If you wanted to value this token based on an earnings multiple (analogous to P/E) of say 20x, you would apply it to this net income number. $900mm x 20 = $18bn. Nice and easy.

As noted above, we also assumed 100% token ownership so as to isolate the asset’s ability to generate income vs. its utility value as a currency. However, an alternative scenario to consider would be if there remained a subset of holders who own the token and keep it un-staked, perhaps even paying inflation to token stakers. This should only occur to a meaningful extent if they derive some utility value from the token outside of its ability to generate income. If this is durable, then we would need to factor this into a more comprehensive valuation model. Also note that LSTs should in theory mostly break this tradeoff, further complicating the analysis.

Now let’s dig into those operator payments, because that’s where the nuance lies. We assumed a flat number of $100mm which stayed constant both before and after the investor purchased all the tokens. You might ask though, couldn’t they cut costs? Maybe this network had a million geo-distributed independent operators, and the new investor could consolidate operations. Technically, yes that is the case. However, it is fair to say that if users wanted a decentralized, censorship-resistant network, then they would no longer be willing to use this centralized network.

This is the price of decentralization. This investor would need to keep paying these decentralized and independent operators if that’s what’s required to keep the REV coming in. In reality, this is a very difficult number to assess. What is the marginal value provided by additional network operators vs. the marginal cost added, and when does that start to decay? There isn’t a clear answer, and it certainly doesn’t map across different projects. There are plenty of protocols where the redundancy isn’t adding user value, and perhaps it’s fine to completely centralize operations to provide the best product at the lowest cost.

This is also where we need to consider taxes. We didn’t assume any taxes in the example above, but this is where they would come out of.

- If this investor lived in a jurisdiction where that income is taxed, then they would have to pay taxes on the $900mm. Perhaps their post-tax net income is something like $700mm.

- Even worse, imagine that this protocol has very high issuance (equivalent to billions of dollars p.a.), all of which goes to stakers. This investor cannot change the inflation rate even if they buy all the tokens. Unfortunately, their jurisdiction taxes this all as income, even though it’s just a redenomination. They may end up with a tax liability which is higher than their profits!

- If another investor lives in a jurisdiction where none of this income is taxed, they could realize the full $900mm, and so they will simply value it based on that.

To keep this example relevant to our decentralized networks (e.g., Bitcoin, Ethereum, Solana), we assumed here that this tax looks like a dividend tax (and not a corporate tax), where its payment depends on the jurisdiction. Now, if someone actually bought all the tokens, and let’s say they also centralize all of the operations, then maybe this just starts looking like a business where corporate taxes would be applicable. If this is a company with its own jurisdiction and corporate tax liabilities, then obviously this changes the tax considerations.

In reality, I’m not expecting anyone to go buy all the ETH out there and put it all on their master validator node. But it simplifies the thought experiment. That market of many different investors should still in aggregate have the same valuation considerations.

Now, as a decentralized network with what potentially looks like dividend taxes on staking rewards and not corporate taxes (which are inherent to the entity and taken out before returning value to asset holders), then we should note the important distinction again of this number vs. operator payments. We discussed how those operator payments are unavoidable costs to the token, and how those must be spent by anyone who wants to earn the profits generated from users.

Still, I think it’s useful for us to estimate the tax burden on token holders going forward. This could be a unified line item similar to operator payments estimated across all token holders. It would of course be impossible to calculate perfectly. You’d be trying to apply a weighted-average tax rate on rewards received depending on where you think they’re held and received, and what tax rate is applicable. Even a very rough estimate (say pick 20%) applied to TEV will demonstrate though how inefficient paying out excess rewards can be, particularly when it’s primarily new issuance if it’s taxable. You can easily end up with token holders in aggregate paying more in taxes than they generated in net income. Currently, taxes are in practice a real expense that many token holders are paying out today. Hopefully we get more clarity and reasonable tax laws over time. If you care about having the broadest possible appeal to potential token holders, taxes are at least something to consider.

Sustainability – Security & Profitability

These types of financial metrics often end up in a debate of whether these networks are sustainable or not. Is Ethereum sustainable if it’s net inflationary long-term? Is Solana sustainable with a higher issuance rate long-term?

People will talk in circles here because “sustainability” is often poorly ever defined. So let’s be concrete. All PoW or PoS networks are fundamentally “sustainable” in that permissionless operators will always be incentivized to run them so long as users are willing to pay a nonzero amount of money to use them.

- If REV ≥ expenses required by operators, then rational actors can always operate the network without any external capital support

- If REV ≤ expenses required by operators, then rational actors must reduce their costs (e.g., reduce hash rate) or get an external capital injection (e.g., token holders pay inflation).

In a company, indefinite capital injections from equity holders with no expectations of future profits would presumably be unsustainable. Equity holders generally supply capital to companies operating at a loss because they expect them to eventually generate profits. If they’re with certainty always going to be unprofitable, you won’t get funding.

In a cryptonetwork, token holders would also be unwilling to supply capital at a loss indefinitely if the token’s only value is derived from its ability to generate profits in the future. However, this gets into the unique properties and value capture mechanisms of crypto – tokens may have value capture outside of their ability to produce income.

Bitcoin is the clearest example – BTC holders are willing to accept inflation as a pure expense with no expectation of future income rights. You could also easily imagine Bitcoin having a 1% inflation tail programmed from the start, and perhaps BTC holders would happily hold it. That would happen because BTC holders derive sufficient utility from holding the token in some way. They want the best censorship-resistant digital store of value. Holding BTC and paying inflation to operators is economically comparable to a user submitting a transaction to the network which pays fees. Token holders are users too.

But let’s put that alternative utility aside, and assume again that we have a network where investors hold the token for the sole purpose of generating income. They will not hold the token with an indefinite loss. In this scenario, the whole point of these systems is that if REV goes up or down, then operators will adjust their real-world costs accordingly to match it.

- PoW – If Bitcoin issuance went away tomorrow, Bitcoin would continue to operate. Users pay REV, and miners would mine blocks to receive those fees. If issuance disappeared, they would reduce their hash rate proportionally. You may argue that this makes the network not secure enough for your own standards, which is a valid point to debate.

- PoS – Imagine a PoS network with 1mm validators, costing $100mm p.a. to run. Users pay $200mm p.a. in REV, and the chain issues $800mm in tokens p.a. to stakers. Operators take a 10% cut on TEV ($100mm here). The “profit = fees – issuance” proponents will say this is unsustainable: $200mm fees – $800mm issuance = $600mm loss! This doesn’t hold up. You could send inflation to 0 in the example above, and everything would be fine. Operators will simply adjust their commission rates in response (e.g., take 50% commissions on REV, with $100mm to them and $100 profit to token holders). Even if REV dipped much lower than operator expenses, some of them may just drop offline to reduce the net operating expenses. Maybe some token holders also decide to remain un-staked, because their opportunity cost is lower now. Maybe you deem that the network is now not crypto-economically secure enough for you, which is again a fair debate to be had.

- Incentives – Imagine an L2 that’s printing tokens crazy, and they’re giving them away to users and apps to come to their chain. They have super high REV as a result. It is fair to argue that this level of REV is likely unsustainable – if and when they need to stop printing money, then it is likely that application and user activity will die down.

As you could see from the examples above, we’re trying to get at the “sustainability” of two related points here:

- Security – In the absence of indefinite subsidization (e.g., from token holders), you need REV to sustainably attract operators and potentially token stakers. An increase or decrease in REV can result in a corresponding increase or decrease in security (in terms of operator decentralization, value staked, and energy used mining).

- Profitability – If a network generates REV in excess of what is needed to pay operators for sufficient security (however it is measured in that case), then token holders can capture the profit. It may be the case that a given network will never generate REV in excess of operator payments, in which case there would be no surplus profit left for token holders.

I think this is all pretty intuitive when we’re discussing Bitcoin, because there are far fewer variables at play. Everyone knows issuance will decline to 0, and then it’s a question whether REV will be high enough and consistent enough to keep miners incentivized to act honestly in securing the network. Bitcoin’s security in the face of a declining block subsidy has been covered at length for many years.

The sillier conversations have been happening on the PoS side. There are a lot more variables at play to get confused over, and we all want our own bags to be special. But we need to stop looking at silly metrics then drawing incorrect conclusions around sustainability. It’s silly to say that Solana is unprofitable or unsustainable. At most, you can argue that if issuance was reduced and the SFDP program went away, that the validator composition would look a little different, they’d charge different rates, and the stake rate might adjust. But it would continue as it does today to generate tons of value far in excess of what is needed to pay operators, and the remaining profits could accrue to SOL holders. REV > operator expenses. We need to point to the specific conditions which may or may not be sustainable.

It’s also funny because the conversation is super contentious and confusing in PoS world, but that’s also where it’s the least important:

- Operating expenses to run PoS networks are wayyyyyyy lower than PoW. The cost of running software will continue to approach 0.

- As I discussed in Endgame: Proof of Governance, and many others have before me, the superpower of PoS security is really accountability. If you double sign, everyone knows who you are. We tend to even know their real-world identities. The attacker can be slashed and/or chased down in meatspace. The “cryptoeconomic security” of PoS chains from high value staked is pretty much all delegated anyway. TLDR this PoS security conversation is super overblown and largely a meme past some reasonable threshold (which networks like Ethereum and Solana are wayyyyy beyond).

As a result of all this, it doesn’t take all that much for PoS networks to be secure and then profitable on top of that, even if marginally. Even old PoW chains with like 6 users left are all still hanging around, and PoW chains are more expensive to run and harder to keep secure cheaply. We’ve got a gazillion ghost chains out there which will shockingly never die. They don’t produce a tremendous amount of real surplus value, and they’re probably far less crypto-economically secure than the big chains, but they just keep going.

L1 vs. L2 Financials

While we have focused primarily on traditional L1s thus far, we will now turn to L2s. For our purposes here, we will just draw a simple distinction between L1s and L2s:

- L1 – Network relies on its own dedicated operators.

- L2 – Network relies on the operators of another network. It may or may not have its own dedicated operators in addition to these.

This means we’re focused on rollups here that post data to some other base layer (e.g., Ethereum, Celestia, EigenDA). We’re not focused on examples such as L2s that “settle” to an L1, but have a DAC (data availability committee) made up of its own dedicated operators. These are just L1s with fancy bridges here.

The biggest misconception to dispel is that L2s are a magically profitable design vs. L1s because they don’t have to pay inflation. If you’ve read the article up to here, this should be clear to you why this is incorrect. As we have established, PoS issuance is not a “cost to the network.” It isn’t even a net expense to tokenholders in aggregate.

For both L1s and L2s:

Token Holders’ Net Income = REV – Operator Payments

The difference is that these operator payments do look a bit different for L2s. L1s have their own dedicated operators that are paid from the network’s own TEV. L2s just recycle the operators of another network. We’re primarily concerned with the data cost here. L2s post all of their data to some other DA layer. L2s need to charge fees which account for paying those L1 operators. That means that L2s just need to also send some portion of their TEV to base layer operators. The L2 may also have to reimburse their own operators (e.g., sequencers) in addition to paying L1 operators for DA costs.

Embedded in those L1 operator costs should be the same thing that it would cost you if you had your own operators. The L1 operators need to be decentralized, buy the required hardware, provision enough bandwidth for your data, pay employees to run the infrastructure, etc. The cost of posting data to this L1 should also expect to have an embedded capital cost (i.e., profit going to token stakers) if the L1 is expected to be crypto economically secure with token value derived from profits to token holders. Still, there are likely to be cost efficiencies from reusing an existing L1 operator set vs. launching your own large dedicated operator set.

There are clearly differences, but they have the same general shape. Let’s take it a step further. What if you wanted stronger pre-confirmations on your rollup (assume this is not a based rollup) rather than a centralized sequencer. Well then you may implement a PoS sequencer set, reintroducing economics that again look even closer to an L1. Or, what if you want to subsidize operators’ costs so that you can undercharge users while your chain gets off the ground? Again, you can achieve this with token inflation, much like any L1.

Additionally, we shouldn’t just focus on launching a new L1 vs. launching a new L2. An equally relevant comparison is launching your own L2 vs. deploying a smart contract on an existing chain. You get the same benefits of recycling infrastructure. All have their own considerations, but nobody is cheating the fundamental simple point that any chain should generate value in excess of the operational expenses required to run the chain if you want a profit for stakeholders.

Finally, I want to double-click on a point we touched on earlier – new token issuance used for incentive programs. While we don’t see this on most of the major L1s (e.g., Bitcoin, Ethereum, Solana), we do tend to see this at significant scale on L2s. Unlike L1s using issuance to incentivize token holders to stake rather than hold idly, these incentives being issued to non-token holders are real expenses to all token holders (with no offsetting income), reducing their net income.

Value Capture Mechanisms

Productive Capital Assets

So far, this post has focused almost exclusively on tokens’ ability to capture value by generating income streams for their holders. They are productive capital assets. This may very well be sufficient to value most tokens in the long-run. Equity-like analysis will do the trick here. Think DCF and DDM.

However, valuing tokens based on cash flows remains challenging. Even for the blue chips, it’s difficult to make even order of magnitude correct guesses on profitability. We’ve seen wild swings in historical metrics. Then if you try to project ahead, will Solana’s end state be 100k TPS, or 10mm TPS? How much of that will be high-value? Will these networks conduct billions of dollars in onchain volume daily, or trillions?

Even if you could guess at the scale of these networks in the long-run, the distribution of value accrual is uncertain. Network base fees should continue to approach 0 over time. There is no compelling reason why they should retain pricing power far beyond some multiple on bandwidth costs. Raw data availability generally has negligible network effects. Incredible volume will be needed. To earn additional income, you will need to offer priority access to valuable state.

It seems obvious that applications, not general-purpose networks, will capture the majority of cash flows generated in these systems over the long-run. This is already playing out. Apps have all of the leverage and pricing power with the end-customer. There’s still a big question though – how much MEV leakage will these apps leave around for the chain’s native token to accrue? (Assuming it’s not an appchain, in which case there’s no difference). Will applications figure out how to internalize 50% of the MEV they’re leaking to L1 tokens today? 90%? 99%?

The point is it’s challenging to produce an estimate here with reasonable confidence, but that’s fine for now. Even today’s largest networks are clearly still very much at a growth stage. It’s necessary to understand the economics in these systems and your general range of outcomes. We can at least reasonably say that in any scenario, the largest platforms’ native assets (e.g., SOL) are capable of generating profits well into the billions. We already see that, and they’re likely to get a smaller slice of a much bigger pie in the future.

It’s worth noting though that even these blue chip L1 assets are trading at some pretty aggressive multiples based on earnings alone. ETH and SOL are both currently generating very roughly ~$1bn in annualized earnings, but they’re trading at ~$300bn and $80bn FDV, respectively.

So, is the market aggressively pricing in a sizable growth in their earnings yet to come, or is there something else going on? What is justifying these valuations in the hundreds of billions, and how do we get deep into the trillions?

Money

As we mentioned earlier, there are other methods of value capture for tokens. Several popular frameworks have been written here over the years (e.g., Cryptoasset Valuations, Paths to $100T, Ether: The Triple Point Asset). Understanding the ability for cryptoassets to generate income is necessary but insufficient.

Aside from being productive capital assets, you have likely heard some variation of these two other buckets for assets (neither of which are necessarily mutually exclusive with each other or capital assets):

- Consumable / Transformable Asset – Sometimes also classified as commodity or utility value. Cryptoassets offer infinitely programmable, fast, private, censorship-resistant, transfer of value. Use your imagination. If you know anything about crypto, I probably don’t have to sell you on the value proposition here, for example as payment currencies.

- Store of Value (SoV) – BTC is the obvious example. Holders own it as a SoV with no expectations of generating income. Most don’t even plan to spend it or move it at all. It has certain useful properties (e.g., scarcity, fungibility, portability), and it’s generally expected to hold its value over time. It’s worth whatever the market says it’s worth.

Empirically, the market values non-productive SoV assets like gold and BTC already into the trillions of dollars today. The big question for us is can other cryptoassets compete here? Can ETH, SOL, TIA, BNB, DOGE, POL, or whatever else you like be money? Note that I am using the term money incredibly loosely here. Saying your coin is a fungible, divisible, durable, portable store of value, medium of exchange, and unit of account just doesn’t have a great ring to it.

There exists no meaningful technical barrier between BTC vs. the field. Most other networks are obviously even technically more advanced. But we’re focused on the dollars and cents outcome here. Will any of these other assets be used in a similar manner over time as BTC, justifying valuations far in excess of their intrinsic value from producing income? That’s what people really mean by that handwavy notion of “monetary premium.”

Frankly, I think most of it is hopium. I do not think there will be a long-tail of ultra-valuable non-sovereign cryptoassets. Unlike some others though, that is not because I doubt the use case. I believe there is a large and valuable place in the world for BTC, or something like it. That is why I own BTC as a non-sovereign, digital, censorship-resistant, SoV. I just don’t believe that a long-tail of assets will achieve this status. I don’t believe that people are going to seriously store their wealth long-term in the 14th best L1 token because it has a sick new VM.

I expect an extreme power law. By number, yes there will probably be more cryptoassets that have some currency-like properties. But I don’t believe long-term that will justify a multi-billion dollar valuation for the millionth L2 launching as its own little self-proclaimed cryptoeconomy nation-state thing. Cryptoassets aren’t going to all be indefinitely worth 100x what you would expect them to be based on TradFi valuations. If they were, then everyone would stick their equities onchain and make them worth 100x. Likely only a handful could ever achieve a durable monetary premium as a non-sovereign SoV.

Crypto is designed to break down barriers, allowing the best money to rise to the top. We see this behavior in stablecoins, where >99% of stablecoins are US dollars. There isn’t a whole lot of organic demand for fiat currency #109. Many people are artificially restricted from holding dollars offchain, which is a major reason for the success of USD stablecoins. The onchain economy should have better asset portability.

Let’s consider some arguments for each side:

Bitcoin is special. It was the first, and it’s still the most decentralized, credibly neutral, predictable, and reliable network. No other network can match its story, and perhaps no other will match these features.

Also, unlike most of its peers here, BTC makes no attempt to be a productive capital asset. Now, that may sound like a weakness at first. However, the advantage of a “sort of productive money” is also questionable. Let’s say ETH or SOL was gunning for the throne, with a market cap deep into the trillions. This would almost certainly squish the real yield available to near 0. Producing hundreds of billions of dollars in REV seems unlikely. Investors keep fighting over which token is going to generate the most income, and new faster chains just keep coming out. BTC stands alone and unscathed by the debates. It’s a potential pure play. It’s not about how much you earn, it’s about what you’re worth.

Interestingly, Ethereum’s rollup-centric roadmap is implicitly a gambit in this direction. ETH is sacrificing REV to its L2s rather than capturing it all to itself, in return for spreading the moneyness of ETH the asset. It’s unclear if its L2s will win out, or if they’ll continue to aggressively use and spread ETH in the future, but it’s clearly the play. It’s also worth noting that this debate over whether L2s are “parasitic” to the L1 because they capture their own REV is unavoidable. Apps on shared L1s will also continue doing everything possible to internalize as much of their MEV as they can, which is equally parasitic in this respect.

Or maybe we all made a bunch of cool tech that’s just really good at moving around USD stablecoins, but our tokens all go to 0.

It’s always fun watching people try to reconcile current L1/L2 market valuations & debate whether to value them:

1) like equities / on cashflows, or

2) like currencies / store of valueWithout acknowledging option #3 that maybe they’re all just overvalued & going to 0

— Jon Charbonneau (@jon_charb) September 3, 2024

Conclusion

We covered a lot of ground here, so let’s summarize our key takeaways here:

- Cryptonetworks are not companies. Income/expense/profit metrics generally do not logically apply at this level. We can try to assess the profitability of all token holders, and/or subsets of them.

- PoS issuance to stakers is not a “cost to the network,” and it isn’t even a net loss to token holders in aggregate. It is both equivalent income and an expense to different holder subsets, netting out to an ownership redistribution.

- Token issuance used as incentives to non-token holders (e.g., incentivizing ecosystem application deployment) is entirely a direct non-cash expense to token holders (with no offsetting income).

- When taxes on staking rewards are present offchain, they mimic the effects of taxes on dividend payments, not corporate taxes.

- REV (all network fees + MEV tips) is incredibly useful in assessing the real demand to use a given network. In the case of PoS tokens which can receive this value, REV is most comparable to a revenue metric in TradFi.

- Token Holders’ Net Income = REV – Operator Payments. For all the complexities here, this matches our simple intuition. What do people pay to use the network, and what does it cost to run the network?

- Operator payments consist of whatever amount of TEV is paid out to them, typically taken in the form of commission in PoS networks. This reimburses them for real-world costs +/- some profit.

- While it’s hard to ever kill these networks, the sustainability of their cryptoeconomic security and token holder profitability can certainly fluctuate with the value they generate.

- L1s aren’t much different from L2s in terms of our token holder profitability calculations.

Hopefully this post can play a small role in improving our industry standards going forward. We need a deeper understanding of these networks’ economics, and we need more common terminology that we can use to compare them.

It’s admittedly tricky to evaluate these networks, particularly when the financial metrics here are often only part of the picture. Indeed, there are also utility and store of value components to many of these networks. This combination can make them difficult to reason about. Still, the earnings and cash flow style analyses here form the basis of evaluating all of these networks and tokens.

Disclaimer: The views and opinions expressed herein are the personal views of the respective author(s), do not necessarily represent the views of DBA Asset Management, LLC (“DBA”) or its personnel or affiliates, and are subject to change at any time without notice or any update hereto. This post is made available for informational purposes only as of the date of publication or as otherwise provided and should not be interpreted as investment, financial, legal or other advice or an endorsement, offer or solicitation of any kind. Investing involves risk. You are strongly encouraged to consult your own advisors. Some information contained herein may be sourced from third parties, including portfolio companies of investment funds managed by DBA. While the author(s) believe(s) these sources are reliable as of the date of publication or as otherwise provided, they do not independently verify such information and make no representations regarding its present or future accuracy, completeness or appropriateness. For further disclosures see: https://dba.xyz/disclosures/.