Thank you to Julian Ma, Mike Ippolito, and Mike Neuder for valuable feedback and review.

The views expressed in this post are solely my own, and do not necessarily reflect those of the reviewers.

Introduction

Does Ethereum lack a “North Star,” and does it need one?

Most Solana folks clearly think so, pointing to the success of their clear vision for “decentralized NASDAQ.” Similarly, Bitcoiners have a clear vision for non-sovereign sound money (“digital gold”). Celestia has a clear vision for unstoppable apps.

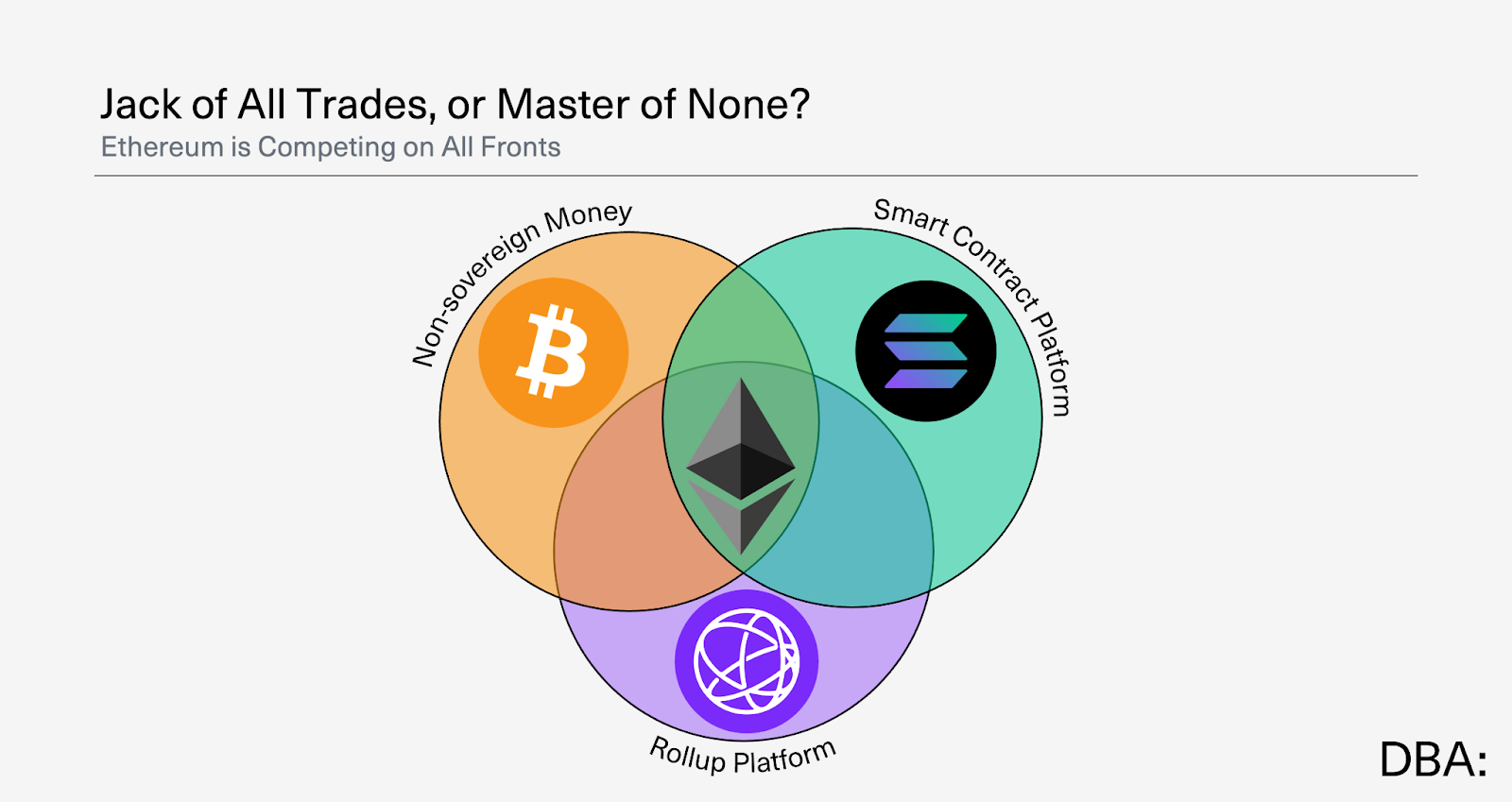

Ethereum is under increasing competition from all sides:

Ethereum is under increasing competition from all sides:

- BTC is better money than ETH.

- Solana is a more performant smart contract platform.

- Celestia is a more performant rollup platform.

Some Ethereans will say “we’re not competing with them”. Well, they’re competing with you, and they’re not shy about it.

This post analyzes the following:

- What is a North Star, and why is it valuable?

- Does Ethereum lack a North Star? If so, is this resulting in coordination failures?

- How does this compare to competitors such as Bitcoin, Solana, and Celestia?

- Does Ethereum need to change, and how?

For context, (at time of writing) DBA is heavily invested in each of the Ethereum, Solana, Celestia, and Bitcoin ecosystems. This includes base assets, L1 applications, L2s, and surrounding infrastructure. We’re even invested in projects that sit at the intersection of many of them (e.g., Eclipse is Ethereum’s SVM L2, and it uses Celestia DA).

I want all four ecosystems to succeed. I hope this post can push forward conversations about how to improve Ethereum by learning from the strengths of its peers.

I also have zero doubt that the broader Ethereum ecosystem will succeed. It’s home to some of crypto’s greatest protocols and applications. However, I think we need to pay closer attention to the roles that Ethereum and ETH will play in that future.

We need to acknowledge the following trends:

- L1 – New asset issuance and activity is leaving Ethereum L1 for alt-L1s (e.g., Solana) and L2s (e.g., Unichain). The desire to keep apps on the L1 is unclear (as is the L1 scaling roadmap, consequently).

- L2 – Ethereum L2s are highly fragmented. A single chain operated by a public company (i.e., Base) is currently set to dominate the field.

- ETH – There is ongoing disagreement over ETH’s role (is it money?), value capture (do we need to scale the L1 for value capture?), and importance (should we care about ETH’s value capture and price?) amidst relative underperformance over the past couple years.

Ethereum vs. ETH

We’ll start by addressing those important motivating questions around ETH.

Critics often use ETH’s underperformance as evidence that Ethereum lacks a North Star. Indeed, ETH/BTC and ETH dominance are near multi-year lows. SOL/ETH continues to hit new all-time highs. Is the market telling us that it doesn’t believe in Ethereum?

There are two reasonable counterarguments for why we should ignore those prices:

Markets Are Not Rational

Markets aren’t perfect at predicting the future. Crypto markets can be especially irrational and short-sighted. Reading too much into short-term price moves is misleading.

Hey Kyle, does Ripple have a North Star?

— Gwart (@GwartyGwart) December 1, 2024

This can all change very quickly, but for now we have several years of ETH underperforming. The fundamentals also line up.

Solana is now surpassing Ethereum on many key metrics, ETH’s regulatory moat is fading, institutions are deploying on Solana, and Solana is gaining traction in real-world use cases. SOL price is downstream of this.

Similarly, you don’t see politicians talking about an ETH strategic reserve, and for good reason. BTC is becoming a global reserve asset. BTC price is downstream of that.

Still, this shouldn’t be a huge short-term concern. It’s unlikely that ETH could be flipped anytime soon. The market is hot now, and ETH has been beaten down for a while. ETH has just started picking up steam in the past week, which hopefully continues. ETH has serious structural advantages and some of the left curve math is in its favor.

That being said, we still need to assess ETH’s importance in long-term planning. The changes we’ll discuss in this post can absolutely impact ETH over a multi-year time horizon.

Ethereum ≠ ETH

Perhaps you just don’t care about ETH at all, and you simply want to see the Ethereum protocol adopted as a technology platform.

This is a reasonable perspective, but the reality is that most people working in the Ethereum ecosystem have a vested financial interest in ETH. Many of you reading this own ETH directly. If that’s you, I probably don’t have to convince you why to care about ETH price.

But let’s put that aside. Let’s assume you are a neutral observer with 0 ETH exposure. You only care about the success of the Ethereum protocol. Even then, you can’t ignore ETH’s value capture and price:

1. ETH’s price is an input to the success of the Ethereum protocol.

ETH’s value increasing helps fund core protocol development (e.g., the EF holds a lot of ETH), incentivizes launching L2s atop Ethereum (e.g., instead of launching an independent L1, or an L2 atop Celestia), creates a wealth effect and provides economic bandwidth for Ethereum applications, and enables a high value to be staked.

TLDR; ETH going up is good for the Ethereum protocol.

2. ETH’s price is a measure of the success of the Ethereum protocol.

To be clear, the market is not pricing ETH 1:1 based on Ethereum’s value provided. You could be more bullish on Ethereum’s adoption than on ETH’s price.

However, they are in practice tied together. The adoption of the Ethereum protocol is a major factor in the price of ETH today. L1 token value capture is still a relatively open topic of debate. ETH is not generally being valued using a DCF, and indeed many believe that cashflows don’t matter much (or even at all) for L1 assets like ETH. It is a common belief that ETH will gain value as a monetary asset. This will be a function of the strength of the crypto-economy built atop Ethereum. In this case, “ETH price” would track “Ethereum’s adoption” quite well.

Overall, the market is pricing ETH to a meaningful extent based on the future expected relevance of the Ethereum protocol and the applications built atop it. This means that long-term price performance actually gives us a pretty decent rough signal of whether the market thinks that Ethereum is building a useful system.

North Stars

What They Are

A North Star is a guiding light which keeps you on track en route to your destination.

In our context here (decentralized protocols), this can be a very specific end use case. Solana’s North Star is decentralized trading. Bitcoin’s is non-sovereign sound money. They’re app-chains in some sense.

Infrastructure platforms’ North Stars may also be more general across end use cases. Celestia wants to enable unstoppable applications. That includes decentralized NASDAQ, decentralized private banking, decentralized Signal, or any other type of verifiable compute.

While Solana’s vision requires one global state machine, Celestia’s vision requires many customizable state machines (rollups). Celestia offers the base product they all need – abundant, verifiable, frictionless blockspace.

All three protocols have a clear North Star, and they offer a clear product in service of their respective end use cases.

It’s also possible for a North Star to be more low-level (e.g., the Merge or the Beam Chain for Ethereum). However, this can be dangerous to have a North Star which is so removed from a clear product offering. We will discuss this more later.

Why They Matter

Many dismiss North Stars as concepts meant for centralized or traditional entities such as companies. This is not true. A clear North Star is a powerful tool for social coordination, especially in more decentralized settings. In particular, I see a clear North Star as allowing us to improve two essential processes here:

- Building (Internal) – A clear North Star makes it easier to internally align the ecosystem on building the best protocol. It keeps builders focused and excited even when times are tough. When everyone knows what you’re building for, it’s easier for everyone to work synergistically (e.g., working together figuring out how to decrease slot times vs. spending time arguing if we should).

- Marketing (External) – A clear North Star makes it easier to pitch to outsiders. This may include pitching the protocol to new builders (e.g., come deploy on Solana because it’s fast and cheap) or its asset to new buyers (e.g., come buy BTC because it’s digital gold).

This is why I disagree with the popular sentiment that Ethereum’s problems would all be solved with a good marketing department. Good marketing is downstream of having a clear mission and purpose to repeat. Narratives are not just made-up stories isolated from reality. At their best, they are distilling for outsiders truths already known internally. Ethereum’s root challenge is that there is fundamentally less internal agreement about what Ethereum’s primary mission is. This is first and foremost a product problem.

Any protocol would benefit from improved building and marketing. On a relative basis though, I find marketing to be especially important for protocols with money-oriented North Stars (e.g., Bitcoin). Building is especially important for protocols with tech-oriented North Stars (e.g., Solana and Celestia).

- Building (Internal) – It’s challenging to build the best platform while your competitors ship order of magnitude tech improvements at a much faster rate. Going toe-to-toe with the likes of Solana as a smart contract platform or Celestia as a rollup platform requires shipping aggressively.

- Marketing (External) – Money is all about the story. If we can’t even agree on the “ETH is money” story ourselves, we can’t pitch it to outsiders effectively.

Ethereum is uniquely fighting on both the “tech-first” and the “money-first” fronts currently. Building and marketing are both essential. A clearer North Star would improve both areas.

We should note though that this North Star stuff isn’t black and white. Assessing the level of clarity and cohesion around a protocol’s mission is inherently subjective. Diverse participants can have differing opinions. There isn’t 100% agreement about what Solana’s North Star is, and there isn’t 0% agreement on what Ethereum’s is. Protocols may even have multiple North Stars.

With that in mind, we can still evaluate each circumstance individually to see how clarity and cohesion impacts coordination. Let’s do that now.

Extremely simple ways of communicating goals enables coordination to scale. When Solana says “increase bandwidth, reduce latency” it aligns the community while creating space for individuals to figure out the details required to make it happen. One could fearmonger and say that…

— Mark Tyneway 🔴 (@tyneslol) November 19, 2024

Ethereum’s Competitors

Solana – Decentralized NASDAQ

We keep hearing that Solana’s North Star is “decentralized NASDAQ”.

This is downstream of Anatoly’s clarity from day 1 that his endgame vision for Solana is to be the world’s best decentralized price discovery engine. If an event happens in Singapore, then by the time that message gets to New York, there should also be a message that a Solana transaction was committed by a block producer in Singapore reacting to this information. Everyone in the world trades on an even playing field.

The protocol is largely built with this clear global finance use case in mind. This clear vision improves the coordination required to build Solana as the best place for it.

In designing any infrastructure from first principles, you would answer the following:

- Why are you building? What’s the end use case?

- How will you enable this use case? What properties does this require?

- What exactly do you have to build to provide these properties?

For example:

- Solana wants to build infrastructure to facilitate global decentralized trading.

- This use case requires maximum throughput and minimum latency.

- To provide this, Solana is building one global state machine synchronized at the speed of light. Increasing bandwidth and reducing latency (IBRL) requires specific upgrades such as asynchronous execution.

We should also note that Solana can (and does) power many use cases other than pure trading (e.g., social apps). There’s also a realization that not everything will happen on Solana L1’s single state machine, as evidenced by recent conversations around “network extensions” (a.k.a. L2s).

Importantly though, neither of these points are currently detracting from or conflicting with the aforementioned North Star. Solana’s undisputed priority is for the L1 to natively host as much activity as possible, with a focus on financial use cases (e.g., trading). Most “consumer” use cases are just derivatives of these core functions anyway.

This use case requires maximum performance, so Solana core developers (e.g., Anza, Firedancer, Jito) don’t sit around debating if they should increase bandwidth or reduce latency. They only work together on how to achieve it within their constraints.

IBRL works because it can rally the troops into a singular effort. The barbarians are at the gates. Our city will be burned to the ground and our children will be sold into slavery unless the next release has more L1 capacity and lower end to end L1 confirmation latency.…

— toly 🇺🇸 (@aeyakovenko) November 22, 2024

Celestia – Unstoppable Apps

Similarly, Celestia has a clear vision which is downstream of an opinionated founder, Mustafa. This includes explicitly defining the core values of the Celestia social layer. The community will decentralize and evolve over time, but culture always comes from the top.

Celestia’s North Star is to enable unstoppable apps. This is broader than Solana’s vision. Celestia is less opinionated about optimizing for “decentralized NASDAQ” vs. “decentralized private banking” vs. “decentralized Signal.” Celestia wants to make the whole internet unstoppable. Build whatever.

Unstoppable apps are those which don’t break under stress from scaling demands, censorship, or faulty operators. Walking through our steps again:

- Why are you building? What’s the end use case?

- How will you enable this use case? What properties does this require?

- What exactly do you have to build to provide these properties?

Celestia’s design make a lot of sense here:

- Celestia wants to enable unstoppable applications.

- Unstoppable apps require abundant, verifiable, and frictionless blockspace.

- This requires millions of customizable rollups that feel like 1 global state machine. Celestia’s mammoth blocks provide abundance. ZK + (DAS) light nodes provide verifiability. Lazybridging (fast blocks + ZK interoperability) unites it all to make it frictionless.

You may also notice that mammoth blocks = increase bandwidth, and fast blocks = reduce latency. Celestia’s goals pretty much boil down to IBRL + verify.

Bitcoin :: Digital gold

Solana :: IBRL

Celestia :: 1GB blocksFocus and simplicity is a superpower. iykyk

— Nick White 🦣 (@nickwh8te) November 20, 2024

While Celestia is less opinionated about end use cases vs. Solana with trading, that obviously doesn’t mean that Celestia rollups can’t compete for trading. Quite the opposite. Celestia just takes the view that developers need even more control and customizability to build for their specific use cases than one shared state machine (e.g., Solana) can afford them. Developers should own their execution environments. So, Celestia only concerns itself with providing the minimum requirements for any decentralized application – a verifiable consensus and data network.

For example, despite Solana’s IBRL, rollups can achieve lower latency. This can be beneficial for many trading use cases. Rollups can give near-instant pre-confirmations (e.g., with less decentralized consensus) prior to the more decentralized base layer’s consensus. This is simply a different product than a single state machine operated by many geo-distributed concurrent block producers. Both offer unique advantages.

Celestia’s focus from the start is a competitive advantage vs. other rollup platforms such as Ethereum:

- Celestia already has DAS light nodes.

- Will continue to have bigger blocks.

- Will have faster blocks. Currently SSF with 12s slots, moving to 6s soon, eventually sub-second.

- Will have ZK accounts enabling lazybridging for interoperability across rollups.

Btw this is @CelestiaOrg

Already has SSF

1 second block times next year

Enshrined ZK verification (SNARK accounts) is ~enshrined zkVM https://t.co/EB4emAVakC— Uma Roy (@pumatheuma) November 24, 2024

The technicals are starting to be reflected in the fundamentals:

- Celestia powers high-performance alt-VM rollups such as Eclipse (SVM) and Movement (MoveVM). They demand max-performance DA beyond what Ethereum can provide.

- Celestia powers unique unstoppable apps such as Payy (private banking and payments) and Prism (encrypted messaging).

- The Celestia-native ecosystem is just starting. Astria is set to build the “Celestia-native Superchain”, with chains such as Flame (DeFi) and Forma (NFTs). The Sloths show Celestia’s community starting.

- Celestia just crossed $1bn total value secured (TVS).

- Celestia is up to a ~40% market share in DA posted vs. Ethereum’s ~60%.

Bitcoin – Digital Gold; Electronic Cash

This is an easy one. Even the haters like Kyle get it:

“Even ironically Bitcoin has more of a North Star than Ethereum. And Bitcoin’s is it is inert, it is digital gold. Like I can say digital gold is dumb or whatever, but even I, as someone who understands Bitcoin and hates it, can acknowledge the product as it exists today, and more importantly as it has existed for like the last 10 to 15 years, is in fact oriented around the thing it claims to want to be. ETH I don’t even think has that.”

Bitcoin’s narrative has certainly evolved since its launch, and some visions have even conflicted at times. However, these visions have generally maintained a clear focal point – BTC as a SoV and/or MoE. As Rick Dudley described years ago:

“Bitcoin is a single application chain… It’s basically a payments network.

And even though they have you know debates to the death whether it’s a store of value or a medium of exchange, at the end of the day everyone kind of agrees… that in order for Bitcoin to work it has to do some of both of those things. It’s kind of irrefutable: it has to store some value, and it has to do some medium of exchange or else neither one of those features actually works.

So when you’re having a dispute in Bitcoin… at the end of the day in the Bitcoin community you can say, are we making it a better store of value? Yes or no. Are we making it a better medium of exchange? Yes or no. And that’s gonna ground the dispute.

But because Ethereum happened after Bitcoin and is more than Bitcoin necessarily in some meaningful way… Ethereum kind of loses that grounding. Right so if you look at the Ethereum narrative it very much starts with this sort of medium of exchange narrative of Bitcoin. Well we can just augment the medium of exchange capabilities of Bitcoin with this more programmable money. Then you sort of have this world computer narrative.”

Major conflicts have also been resolved decisively (as in the block size war) with each side going their way for the better.

Competition is a Spectrum

Ethereum vs. Solana

Competition is a spectrum. Protocols compete more and less on various dimensions.

For example, Solana is not meaningfully competing with Ethereum as a rollup platform. There are some “network extensions” (L2s) starting to pop up on Solana, but they’re clearly a footnote in the broader Solana ecosystem. They are not a primary consideration being accounted for in designing the Solana protocol.

Execution is another story:

I am competing with ethereum for the best decentralized execution platform. https://t.co/EyPjU3gFfw

— toly 🇺🇸 (@aeyakovenko) November 23, 2024

Conversely, competing execution environments may have symbiotic effects at times. For example, some Ethereum L2s may expand the “moneyness” of ETH if they use the asset heavily. Others may be strictly parasitic, stealing activity that would otherwise happen on Etheruem L1, without using ETH at all. It’s a spectrum.

This also highlights how Solana could become more symbiotic with Ethereum – it could become an Ethereum L2. You don’t even need anyone’s permission to do this. You could simply create a data validating bridge between Solana and Ethereum. However, there are a few issues here today:

- Scale – Ethereum cannot currently fit all of Solana in its blobs. Solana has too much throughput.

- Cost – It’s unclear if users want this enough to pay for it. There are real costs (posting data onchain + offchain proving + onchain proof verification).

- ETH – It’s unclear how much users really want to export ETH to other chains such as Solana, even if they could do so with minimal trust assumptions. Perhaps current L2s using ETH heavily are not representative of broader user demand. They may be a byproduct of early challenges which are disappearing (e.g., difficult to bridge BTC and USDC or abstract gas for users).

Ethereum vs. Celestia

Unlike Solana, Celestia presents meaningful synergies with Ethereum in practice.

Celestia is used as a DA solution for Ethereum L2s such as Eclipse that require maximum performance. While they don’t pay fees to Ethereum for DA, that’s a perfectly acceptable tradeoff. Ethereum is generally valued more as a monetary asset than a cash flowing asset, and DA fees are low regardless.

As Justin noted on his recent Bankless podcast on Ethereum’s Three Front War:

“The way that I see it is that Celestia is in some sense a collaborative player with Ethereum because it provides overflow DA when there isn’t sufficient capacity on the L1…

I think we can go even further and have L2s where you consume alt-DA as opposed to consuming Ethereum DA. One of the potential outcomes in the next few months is that Ethereum DA is going to become extremely, extremely expensive. Think cents per transaction, or tens of cents per transaction. And I think it should be totally socially acceptable for some of those rollups to at least temporarily move away from this expensive Ethereum DA and use alt-DA.”

However, Celestia’s upcoming addition of ZK accounts will enable trustless TIA settlement, allow TIA to act as permissionless money in its own ecosystem, and enable Celestia to facilitate rollup interoperability. This allows Celestia to compete for a bigger piece of the pie:

“Celestia, initially they started as pure DA, and then they recently… are planning to add more execution… around being able to verify SNARKs on Celestia. And once you have these two components, and TIA the token, yes you have all the ingredients to potentially win this massive endgame.”

Ethereum vs. Bitcoin

Many Ethereans clearly want to compete with BTC head-on. “Ultrasound money” is of course a play on Bitcoin as “sound money.”

However, BTC is undoubtedly in the lead as a monetary asset. It’s far more valuable than ETH, and major nation-states are now even considering building BTC reserves.

Additionally, Bitcoin is getting into the rollup game – BTC will finally become programmable and private. More trust-minimized BTC bridges and ZK rollups are on the horizon with Alpen Labs’ Strata. Still, these BitVM-based bridges are admittedly clunky and carry 1 of N trust assumptions (i.e., they include optimistic SNARK verification). However, potential future Bitcoin soft forks (e.g., re-enabling OP_CAT) would alleviate these issues. This has even sparked interest from Ethereum L2’s such as StarkNet to start settling on Bitcoin in addition to Ethereum.

Ethereum’s North Star

Does Ethereum Have a North Star?

Ethereum has gone in a relatively coherent direction over the past decade, but it certainly does not have the same clarity vs. its competitors here. Bitcoin, Solana, and Celestia all have clearer objective functions. Their respective protocol designs are very clearly catered to achieving them.

I’ve seen countless different answers for what Ethereum’s North Star is. Anecdotally, I was on a panel at a Devcon side event full of core Ethereum community members. One of my co-panelists asked the audience if anyone felt confident that they could clearly explain Ethereum’s North Star – nobody raised a hand.

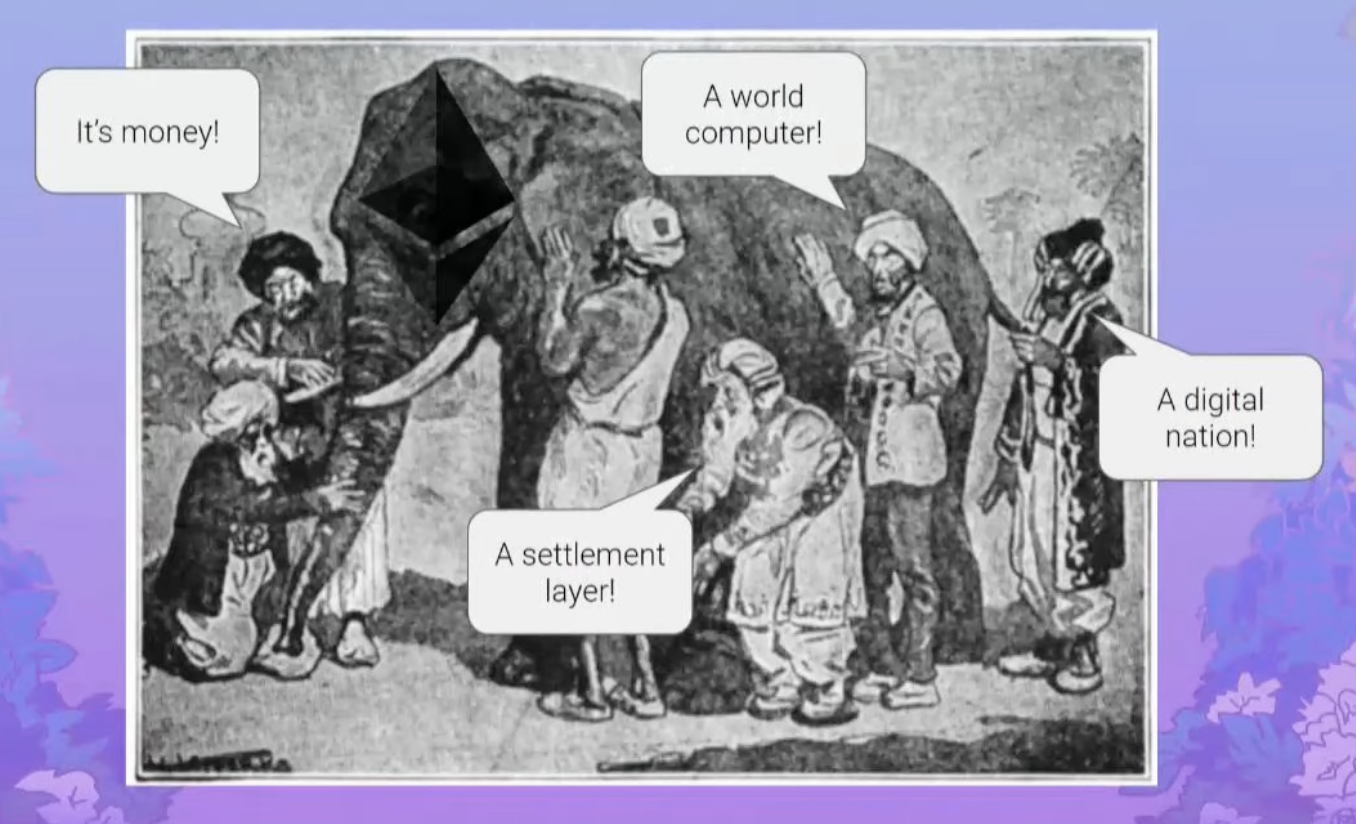

There’s a reasonable argument that this is because Ethereum is very complicated. Tim recently described this at Devcon:

“Ethereum is quite hard to describe… It’s this complex thing and so it leads us to use analogies to describe it… I really like the parable of the blind man and the elephant to think about this. When different people look at Ethereum they’ll see something different, right. Some people will look at it, they’ll see that there’s this asset in the middle, ether, and think of it as money. Other people will see that there’s this EVM, it runs computations, it’s like this world computer. You can think of it as a settlement layer for everything to use as sort of this global ledger. And even extending that to something like Ethereum is a digital nation state.”

Source: The Shape of Protocols to Come, Tim Beiko

However, I don’t think that we can chalk this all up to complexity. It’s not like Ethereum is far more technically complex than Solana. They’re also both capable of performing basically the exact same literal functions.

Ethereans just agree less on the protocol’s core purpose. The difficult question here is what is Ethereum uniquely optimized for doing better than any other protocol? Why do we need Ethereum when we have Bitcoin, Solana, and Celestia?

Does Ethereum Have Multiple North Stars?

More precisely than being technically complex, maybe the issue is that Ethereum just has a complex vision. You can argue Ethereum just has a more ambitious vision than Bitcoin, Solana, and Celestia because it’s trying to do a bit of each. So, maybe Ethereum has multiple North Stars?

What’s Celestia’s roadmap?

1 gigabyte blocksWhat’s Solana’s roadmap?

Increase scale, reduce latencyWhat’s Bitcoins roadmap?

Sound money=====

What’s Ethereum’s roadmap?

All of those things, better, and togetherEthereum will have greater than the sum of its parts

— Brother DavidHoffman.eth 🦇🔊 (@TrustlessState) November 19, 2024

If Ethereum does have multiple North Stars, we need to consider whether this is a problem, and why. More specifically, which of these buckets do we fall into?:

- Synergistic North Stars – This may be a good thing. It’s possible that multiple distinct North Stars actually benefit from being coupled, increasing the probability of success. Maybe you need to balance native asset “moneyness” while also being aggressive on tech development.

- Parallel North Stars – This could be good or bad. This could increase the probability that you picked and developed the right path over time. It’s best if both paths can be pursued entirely in parallel with zero resulting interference or distraction (e.g., if you assume that pursuing two North Stars does not slow down the progress towards either goal).

I think that’s fair if the research streams were competing. But in practice they’re not competing – the people building SSF and the people building preconfs are quite separate and don’t really interfere with each other.

Ethereum ecosystem has many instances of this kind of…

— vitalik.eth (@VitalikButerin) November 20, 2024

- Conflicting North Stars – It’s problematic if two North Stars are in conflict. It’s challenging (sometimes impossible) to pursue multiple visions which have mismatched priorities (e.g., resulting in moving too slow to compete). If you don’t fight it out to pick a decisive direction, then the probability of achieving either goal is reduced.

And while I am a strong proponent of the second path, the reality is that L1 is very slow at executing on it.

With more pragmatism, we could have more capacity on the L1 as well as more blobs. But sadly, this is not the way we do things.

— Dankrad Feist (@dankrad) November 14, 2024

As long as they are not in conflict, yes.

But I would argue that now they are. Many of Ethereum’s processes (multi-client architecture, ACD) were a result of creating a maximally “hard” asset to compete with Bitcoin.

However, they now make it almost impossible to deliver on the…— Dankrad Feist (@dankrad) November 14, 2024

Who Is Ethereum Competing With?

Many within the Ethereum community do not see a conflict between these North Stars, and so they happily embrace the idea that Ethereum is indeed competing with everyone.

Others seem to express a more targeted approach, as Justin recently discussed:

“One of the things that Vitalik shared… is that the L1 is competing with Bitcoin, and the L2s are competing with Solana…

There’s this level of indirection and I think we should kind of embrace the separation of concerns, and the L1 should focus on infrastructure and the L2 should focus on users.”

However, Justin’s roadmap also prioritizes improving the L1 execution layer (e.g., delaying the L1 state root computation, multidimensional gas pricing, ZK L1) in order to ~100x its gas limit over the next few years. Additionally, he describes how L1 pre-confirmations will soon give “faster-than-Solana” transactions. Users will get a continuous stream of intra-slot transaction confirmations.

That sounds a lot like Solana! Solana has a very large execution budget, having made design decisions such as asynchronous state merklization with plans to implement asynchronous execution. Solana validators continuously stream partial blocks (shreds) for low latency.

Those changes sound a whole lot like Ethereum L1 competing with Solana head-on then.

imo an important fundamental trend rn is that Ethereum is trying to become more like both Bitcoin and Solana. https://t.co/74n3FBBmvn

— Jon Charbonneau 🇺🇸 (@jon_charb) November 26, 2024

There’s some disagreement over the competition with Bitcoin as well. Many within the Ethereum community go so far as to say that “ETH is money or the whole thing was pointless.”

Others see a direct conflict between competing against Bitcoin vs. delivering blockspace to power a global decentralized economy. Many of the OGs clearly dislike the focus on ETH as (ultrasound) money:

Nobody gives a fuck what the OGs think

— Vance Spencer (@pythianism) September 20, 2024

Many Ethereum builders also see the tension between these visions, particularly when “ETH is money” breeds a desire for ETH to capture (and potentially burn) value created by the Ethereum protocol:

I mostly agree with this thread. But I think we’re starting to see tension arise from competing ETH narratives and visions

Is the goal of burning ETH to make ETH holders rich or to make the system as secure as possible?

Are we building ultrasound money or a permissionless app… pic.twitter.com/VLfyYbZeqh

— Hayden Adams 🦄 (@haydenzadams) October 19, 2023

This makes it more challenging to embrace and pursue either direction as effectively as possible. Competing head-on with Bitcoin can skew your priorities in a way that makes it challenging to ship the best tech.

We’re left with a lot of big open questions today:

- Should the L1 compete on execution, or leave it all to L2s? If it’s competing, should it be scaled now, or can we just scale it years down the road?

- Should the L1 be fast enough to facilitate useful interoperability between L2s, or do we push that to out-of-protocol solutions like AggLayer?

- Should the L1 provide enough DA for all rollups, or is it fine if a bunch use Celestia because ETH derives value from moneyness (not cashflows) anyway?

- Should value accrual to ETH be factored into these decisions?

And so it’s true we run a real risk of “cosmosification”: The L1 is retreating more and more to its base function, and other projects fill in the gaps.

And as they are building the product, they will ultimately accrue the value. This is in short, Ethereum’s value accrual…

— Dankrad Feist (@dankrad) November 14, 2024

Should Ethereum Scale the L1?

“A big question that any L1 scaling roadmap needs to answer is: what is the ultimate vision for what belongs on L1 and what belongs on L2?”

This is just about the most fundamental question for a chain to answer, and yet it continues to remain largely unanswered in the Ethereum community. That is a problem.

Ethereum execution layer has been in a weird middle ground imo, should prob either:

– Commit to making it better, increasing gas, more client optimization work, statelessness, etc, or

– Yeet everyone off the L1, low gas, extend 30 second block times, etc, Celestia-style

— Jon Charbonneau 🇺🇸 (@jon_charb) January 10, 2024

Ethereum L1 competes vs. other execution environments like Solana today. Many of the applications, use cases, and users are functionally or literally the same across Solana and Ethereum. They obviously make different tradeoffs (e.g., different node requirements), but they absolutely do have substantial competitive overlap.

It’s an open question though whether Ethereum will cede execution to other chains or continue trying to compete here. Doing so would likely require shifting Ethereum’s point on the decentralization vs. performance tradeoff spectrum at least somewhat more towards performance. This means increasing L1 gas limits and reducing latency (faster slots and faster finality) more aggressively. Users want fast and cheap. Long block times are also inefficient for many DeFi protocols (e.g., increasing LVR).

Scaling the L1 may be necessary for value accrual. Vitalik has noted that one argument to scale L1 execution is because in absence of doing so, it is possible that “the economic situation of ETH the asset becomes more risky, which in turn affects long-run security of the network.”

Having an L2 roadmap is still correct, but:

1. It needs to be really done at scale. We should be at 100s of blobs now, not 3

2. It still needs product focus.

3. Scaling the L1 in addition is not optional, if you also want value accrual.— Dankrad Feist (@dankrad) November 14, 2024

However, the popular sentiment is generally that “Layer 1 is not there to be ultra fast. It is not there to do a million transactions per second.” Many even see Ethereum as a B2B chain which is not meant to serve individual users. For example, Justin clearly described this in his debate vs. Anatoly:

“One of the things that Anatoly asked is, as a dev should I launch on L1 or L2? Well I’ll answer that for you. You should launch on L2. There is no future for the L1 directly. The L1 is a settlement layer.”

Many L2 teams also have no desire to see Ethereum compete on execution.

We see that:

- Disagreement over Ethereum’s purpose →

- Disagreement over what properties Ethereum should optimize for →

- Disagreement over what specific changes should be made to Ethereum.

This is reflected in debates around the L1 gas limit, where there have even been conversations about exploring lowering the gas limit.

We see similar disagreement over slot times. Vitalik has previously noted that “I don’t expect the per-slot time to be reduced much in the future.” In fact, many have been concerned over the past few years about serious conversations to increase the Ethereum slot time (e.g., 16s+ under some PBS designs or potentially to more easily implement SSF). While conversations to increase Ethereum slot times have mostly gone away, there certainly isn’t broad support for goals as ambitious as Max’s desire to get to 1s slot times over the next few years.

Justin described in his Bankless podcast debating Anatoly how “one of the things that we’re not ready to do is have these really short block times… and the reason is that introduces ugly timing games.” More recently at Devcon, Justin discussed the possibility of perhaps at least getting down to 4s slot times by 2030 in his unveiling of the Beam Chain.

I personally think it’s in Ethereum’s strategic interest to fight hard to keep plenty of applications (e.g., high-value DeFi) natively on the L1. Ceding execution entirely would give up Ethereum’s strongest defensible moat today. It would end up looking more like Bitcoin (with less desirable money) and/or Celestia (with worse tech for rollups).

My general sense is that most Ethereans also want to keep meaningful L1 execution. However, the common reaction I see is a fear of admitting that Ethereum is competing here. This gives us a path to say “oh, well we didn’t care about execution on L1 anyway, that was never the plan” if and when Ethereum L1 loses out on execution. The result is that conversations such as increasing the L1 gas limit sit around for years, even though we know we can responsibly do it today with negligible tradeoffs. This indecision around L1 execution ends up becoming a self-fulfilling prophecy. Failing to improve the L1 or trying to keep apps there will result in it losing.

Multiple Concurrent Proposers

Related to L1 scaling, recent debates around multiple concurrent proposers (MCP) again highlight Ethereum’s relatively less clear purpose. Solana is largely arguing over whether MCP can provide their desired properties for global low-latency trading, giving anyone in the world equal fast access to financial information. Ethereum conversations have been more unstructured due to the disagreement over the desired use cases and properties to even optimize for. It’s not entirely clear yet whether it will make sense to implement MCP in either protocol (or exactly how), but at least the Solana conversations are generally more targeted. That’s the necessary first step.

On the recent Bell Curve episode on MCP, Mike asked:

“Where do you get the sense that the other stakeholders, like client teams etc.? Where are they falling on this question? Is there broad agreement?”

Max answered:

“On ETH or on Solana?… On ETH I think we’re in a bit of a weird spot in ETH development where we have a lot of different people who want different things, and we need to at least decide what the objective function is. Because I don’t think we even know what the objective function is.

There’s people who want ETH to be money. There’s people who want ETH to be a settlement layer. People like me who want ETH to be the future of finance, and for finance to happen on the L1. There’s people who want to optimize for the L2, and people who want to optimize for the L1…

We’re incredibly fragmented at the moment, and I hope that we can converge.”

Similarly, Gwart recently asked James Prestwich:

“How do you feel then about the current proposals regarding Ethereum scaling? Do you have any reservations about increasing block times or multiple concurrent proposers?… What do you think is a good idea? What do you think is a bad idea?

To which James responded:

“A lot of these are put forward by specific people who have specific goals… My main problem with evaluating them, from a non-technical perspective, from evaluating like what’s good, is I don’t think Ethereum has a consistent view of its own goals, of its purpose. Everybody has a different idea of what makes Ethereum good. And that set of ideas has changed so much over the years and has grown less cohesive over time. The question like what should Ethereum do implies that you have some sort of goal for Ethereum. And in the absence of a clear, somewhat unified, set of goals we can’t really evaluate any specific proposal.

Because we don’t know what Ethereum is supposed to do, we don’t know how to achieve it… We can’t say whether we should have multiple concurrent proposers or whether we should prioritize ILs, or ePBS, or PEPC, or home staking, or whatever. And so the debate gets caught up in a lot of going back and forth about technical ideas, when it’s really a values debate. We’re not really debating MCP, we’re debating what should Ethereum be in the long run. And that’s something that we’ve always been pretty bad at agreeing on, determining, and it’s just gotten worse and worse over the years.”

Settlement Layer

When people do agree on some important key points for Ethereum’s use cases, they’re often relatively loose buzzwords. For example, “settlement layer” is one of the most common “North Stars” you’ll hear. As Gwart put it on his recent 0xResearch podcast:

“I think that Ethereum does have a North Star, okay. What I would agree on is I don’t know what it means. Their North Star is the global settlement layer, for robots, if you’re Mike Neuder, it’s for robots, but it’s the global settlement layer.”

When you push on what “settlement layer” means, you will get many different answers, many of which are just poorly defined abstract properties rather than a literal description of what the system is doing. Agreeing on a term which we then don’t agree on the meaning of isn’t much better than not agreeing on a term to begin with.

For example, Bitcoin, AggLayer, Base, Celestia, Astria, and a bunch of other protocols are also “settlement layers.” However, they obviously diverge meaningfully in their purposes, as reflected in their divergent architectures. So, what is Ethereum trying to do here then?

- Is Ethereum trying to be a highly functional “settlement layer” that facilitates fast commitments and interoperability between chains? This looks more like AggLayer or Astria. If so, this requires a fast consensus. That’s why even Celestia has been updating its roadmap post-launch to reduce its block times from 12s to 6s and eventually sub-second.

- Is Ethereum trying to be a very minimal “settlement layer” that provides a final slow verification of other actions done elsewhere? This looks more like Bitcoin, as it evolves with rollups such as Strata being built. This makes sense if the core purpose of the base layer is to issue decentralized money. Then other chains necessarily must settle to the base layer because it is the ledger of record for that asset. If this is the case, then maybe it’s fine to be incredibly slow, and leave faster commitments (including those required for fast sequencing and interoperability) up to external protocols (e.g., AggLayer and Astria). There’s also an open question to just how important coupling DA with settlement will be. Not every L2 will be able to use Ethereum DA, so is Ethereum ok with lots of alt-DA ETH L2s since they can increase ETH’s moneyness anyway?

The first vision is more tech-first, and the second vision is more money-first. “ETH is the core product, the market can figure out the rest.” Depending on your interpretation of Ethereum’s purpose, you will draw radically different conclusions about what to prioritize. Both directions are valid, but we need to agree on which we want if we want to make it a reality. We can’t properly assess tradeoffs if we don’t know what the end goal is.

Maybe we just need to stop saying settlement layer.

Ethereum’s Mixed Priorities

All of this ties into my point from earlier that efficient protocol development is downstream of a clear North Star. Lack of clarity over Ethereum’s purpose continues to result in more disagreements around how to improve the protocol. It becomes challenging to agree on which upgrades are desirable and how they should be prioritized.

As recently discussed by Mike Neuder on The Gwart Show:

“Not everyone agrees on what the right priorities are, and there’s no clear obvious next thing that Ethereum should be building towards.

And this is actually reflected in the actual planning around Pectra. Pectra is the next hard fork that comes after 4844. So 4844 was in April of this year, so it’s already been six months, the time has passed, and we were doing Pectra planning at the beginning of the year. Everyone’s throwing out EIPs, there’s a sort of cadency and beauty contest lobbying process that goes around in terms of everyone deciding what they’re going to signal support for or not.

And this was like January through March of 2024, and now we’re in October, and Pectra still isn’t totally finalized. It’s like 10 months have passed and still new things are getting proposed, proposals are getting removed. Pectra actually got split into two different hard forks, they’re calling it Pectra A and Pectra B. Pectra A probably won’t actually happen until maybe at the best like end of Quarter 1, 2025.

So just in terms of timing here I think that’s what people are starting to recognize. These things are taking a really long time.”

Ever since the rollup-centric roadmap was revealed, the Ethereum community has broadly agreed that “L2s are cool.” However, I don’t think there’s been a whole lot of agreement beyond that regarding what Ethereum’s place in that world is.

As a result, we are seeing Ethereum L1 lose its dominant position. Its previously wide lead is shrinking. Solana is picking up serious activity, rivaling or even surpassing Ethereum on many key metrics. L1 apps staying within the broader Ethereum ecosystem are starting to migrate to L2 (e.g., Unichain).

Whether or not a protocol can afford to be slow in development is case-dependent. Bitcoin can afford to be slow because money is all about network effects, and BTC has a gigantic lead. Even still, there’s frustration in Bitcoin at times that things are moving too slow.

Ethereum could afford to be slow early on when it commanded a massive lead over competing smart contract platforms. However, Ethereum has stronger competition now. It may not be able to afford to move as slowly as it has in the past.

It doesn’t make it impossible. It just means the timescales are incredibly slow, which we cannot afford anymore.

— Dankrad Feist (@dankrad) November 14, 2024

“Peacetime in business means those times when a company has a large advantage over the competition in its core market, and its market is growing. In times of peace, the company can focus on expanding the market and reinforcing the company’s strengths.

In wartime, a company is fending off an imminent existential threat. Such a threat can come from a wide range of sources, including competition.”

– Ben Horowitz, The Hard Thing About Hard Things

The Merge, The Beam Chain, & The Roadmap

As discussed earlier, the ideal North Star is generally a use case (or a general class of use cases) that requires clear properties. This allows you to confidently build the best product in service of it.

However, it is also possible for a North Star to sit at another level of abstraction. For example, the Merge arguably served as Ethereum’s North Star for a period of time. Justin’s proposal for the Beam Chain, a bundled consensus layer upgrade, could serve as a new North Star. He described its motivation:

“One of my kind of meta goals for the Beam Chain is to introduce a new meme that gets the community excited and helps the developers in particular kind of all come together and work on a common goal. Like right now we don’t have a clear sense of a quote North Star.

There’s a lot of discussion around what needs to be prioritized in the next few forks, and I think it would be good and healthy to basically draw a line somewhere in the roadmap. Say, okay these are items that we want to do in the next few years because they’re high priority, they’re low hanging. And then there’s another set of items that are you know ambitious, more likely than not require kind of a clean slate approach. Let’s just bundle all of these things together, minimize the use of governance, and basically ship everything in one go. And so on the topic of minimizing governance I think of it as a governance batching optimization.”

This is very reminiscent of the Merge. For several years, the Ethereum community had a clear goal that everyone was gunning for. Everyone knew what the priority to ship was, and they were laser-focused on getting it done. It took a few years, but ultimately it was executed flawlessly.

However, a North Star which lacks a clearly envisioned use case can be dangerous.

The Merge and the Beam Chain both fall into this bucket. On the one hand, they may effectively coordinate the “building” point I noted that North Star’s are valuable for. The Ethereum developers who coordinated the Merge pulled off an amazing feat that required immense focus. They worked for years at a very specific goal, and they were successful.

However, it is dangerous to optimize for any specific properties or upgrades without a clear vision of a use case, because it may well end up that you just optimized for some completely arbitrary and complicated things which are not in fact useful. That’s certainly not to say that the Merge was a bad idea, but rather to make it clear that we always need a deeper purpose.

This is also why, as we saw with the Beam Chain reception, a North Star which lacks a use case is at high risk of failing on the “marketing” front. Everyone wants to know what the heck all this complicated stuff is useful for. “Ethereum is the chain that by 2030 will implement a bundled upgrade of SSF, 4s slot times, ZK consensus, ….” is not an inspiring message to users, investors, or new developers. This is emblematic of why Ethereum’s North Star often feels like “we do technology… we are on the frontier of hard research.” People want to know but why?

Again, I think a lot of stuff in the Beam Chain proposal is really cool. It may very well make sense to bundle it together and do it in one go. However, agreeing on these specific proposals is still downstream of us agreeing on the general vision we all have for Ethereum. It will remain challenging to agree on what upgrades should be prioritized here if we remain unable to articulate the base motivations.

What is Ethereum’s core mission?

This should also make it clear why something like Vitalik’s roadmap cannot serve as a North Star:

”eric, who radicalized you?”

This tweet. This tweet radicalized me pic.twitter.com/Qce5VOxiRf

— Eric Wall | BIP-420😺 (@ercwl) November 13, 2024

What Should Ethereans Do?

Nothing

ETH is a ~$450bn asset, the L1 is hosting some of the most valuable activity in crypto, and the rollup-centric roadmap has been incredibly successful in many respects.

There’s a valid argument that Ethereum doesn’t need to change. Ethereum is incredibly successful even with more ambiguity than its competitors have today. There is no fundamental rule of the universe that a clearer and more agreed upon endgame 100% correlates to winning. Visions change, and even Bitcoin has evolved its narrative over time.

All of these are possible:

- It’s possible that Ethereum is directionally pointed in the right direction even if it’s not easy to express today.

- It’s possible that Ethereum’s network effects can carry it to the finish line even if it takes a slower path vs. competitors who ship better tech faster.

- It’s possible that Ethereum doesn’t need to be the best at any one thing. The many domains on which it is competing with others 1-on-1 (e.g., sound money vs. Bitcoin, financial rails vs. Solana, rollup platform vs. Celestia) may be synergistic, such that being #2 at each of them = winning at all of them because they benefit from being bundled.

That being said, we can’t deny that Ethereum has relatively less clarity and agreement in its purpose vs. competitors. It is surprising to me that this is still the popular sentiment I see from many Ethereans. Once we acknowledge this, we can have a productive conversation about whether this needs to change, and how.

Are you saying we need more Alignment ™️ 😛?

Jokes aside, I think we pretty much agree. 🤝

Twitter compresses these takes lossily..!

— timbeiko.eth (@TimBeiko) October 27, 2024

Talk to Your Customers

Personally, I believe that Ethereum does have a “North Star” problem here. The coordination problems we have seen in this post all point to this. Ethereum probably can’t afford to be as slow and fragmented as it has been in the past.

Let’s say we agree now that it’d be good for Ethereum if we rallied around a more cohesive North Star. How might we accomplish this?

First of all, we should pay more attention to users and applications. As noted before, designing any infrastructure from first principles should ideally start with some clear use case, or at least a general type of use case. Skipping that step is making it difficult to decide what to prioritize as a result. This is often a gigantic disconnect in large parts of the Ethereum community.

For example, there is a very common notion that Ethereum’s North Star is home staking. That is insane. Protocols aren’t made for stakers. They’re made for users.

A protocol whose sole purpose is to allow people to stake from home, with no thought about what else the protocol will be used for, is basically a ponzi doomed to fail. Decentralization and solo staking must be means to a clearer end, not the end goal themselves.

We need more focus on users and the applications they use.

ACD is super conservative. Most core devs are very far away from users, and only interact with stakers, so essentially represent their opinion. And there is no counterbalance.

— Dankrad Feist (@dankrad) November 14, 2024

Potuz you have been working now for a long time on ePBS. If successful every transaction will pass through this market structure. Do you not think it is important to understand how applications might be effected by this change? https://t.co/q2hCJjc3hq

— Max Resnick (@MaxResnick1) November 11, 2024

They are also involved in making decisions on ACD though, which is practically speaking Ethereum’s only decision making organ.

In order to do that knowing what the protocol is used for is beneficial.— Dankrad Feist (@dankrad) November 11, 2024

As Kyle described on his recent Bankless podcast:

“I would talk to your customers. Marc Zeller… recently… said I’ve never spoken to anyone who works at the Ethereum Foundation. I’ve never spoken to Vitalik. None of them have ever reached out to me. And he today is the primary person stewarding Aave. And Aave is the #1 application on Ethereum in terms of sheer dollars in the system… How can the core people who are supposed to be building the future of Ethereum do so without talking to their core constituents?

The Solana Foundation, there are people who are like the DeFi team, and the DePIN team, and the stablecoin team. There’s very obvious groups of people who are designed to interface with all these various stakeholder groups, take their input, and figure out what you need to build and stuff. And you see that manifest very clearly with token extensions and other things that they’ve launched are directly an output of those functional units out of the Solana Foundation.”

solana is not strong due to speed or cost

it’s strong because it embodies the startup ethos more than any other

build for the customer that exists, release fast, simplify marketing — production is the ultimate test

— xrp mert | helius.dev (@0xMert_) November 24, 2024

Wartime CEO

Ok, so we went around and got a better understanding of what the users wanted. Now we need to take in that information, and decide what product Ethereum should prioritize shipping. This will require a lot of social coordination to align many stakeholders. How do we achieve that?

Increasing efficiency here would probably require more top-down alignment. This can come from a central organization (e.g., the EF or Consensys) taking a more opinionated and active role. It can also come from an individual leader.

More concentrated leadership certainly makes it easier to align everyone. This is a benefit for Solana today, as Prestwich described in that same Gwart podcast:

“Solana has the advantage of having a very small number of individuals who set the goals in the roadmap, and you know a marketing director, and all that kind of thing. Ethereum has opted out of exercising you know centralized control in most cases, or of like directly exercising it. Whereas Solana people have control, they build things, they set roadmaps. Solana is more culturally centralized. People look to the company or the foundation more for direction on what Solana ought to be…”

This contrasts to Ethereum:

“In Ethereum there is a much wider range of opinion options out there for you to choose from… So Ethereum, for better or worse, has attempted to decentralize the community. The EF has mostly opted out of organizational opinions on technical issues, on what Ethereum should be, etc. And without that organization at the front with a consistent message keeping everyone else moving in the same direction, you’re going to have a big discoordinated community, and you’re going to not know exactly what Ethereum’s goals are at any moment…

Talking about Ethereum’s purpose… Vitalik has ideas about what Ethereum should do, and he embeds those ideas into his technical designs, and into his roadmaps… Vitalik has ideas about what Ethereum is and what it should do, otherwise he wouldn’t be making technical designs at all. He is ideologically motivated to build Ethereum into something amazing, and to realize some vision where Ethereum is transformative to society, and that I think is extremely admirable on its own.

What I don’t like is that he won’t generally tell us directly what those ideas are, and his ideas have a frame dragging effect. Vitalik’s ideas, that we aren’t even directly observing, are pulling everything else along with them in specific directions. So when people are talking about the roadmap, the Merge, the Purge, the Surge, those are Vitalik’s thoughts about something we should do, for reasons that are in his head, that we don’t fully know. And people treat it as an official this is what we will do, and it becomes you know this cargo cult roadmap of people talking about the Surge without even knowing why those things are valuable.

So it’s this very strange setup where Ethereum wants to be this decentralized community, but there are still a small number of leaders whose word carries a huge amount of weight but aren’t clearly communicating and refuse to exercise power.”

This power vacuum results in many other entities exercising power. In particular, Ethereum’s L2-centric design and tendency to push technical complexity out of the protocol also pushes political power out of the core protocol. We don’t just have L2s taking over Ethereum’s execution, they’re also taking more political control. The same goes for EigenLayer, AggLayer, and others.

These external protocols generally have their own tokens and financial interests. These projects (and their investors) may have incentives that do not align with the Ethereum core protocol (and ETH). For example, L2s may have very different incentives around whether the L1 should scale vs. the incentive that ETH holders have.

This contrasts to more technically integrated protocols (e.g., Solana) which internalize more complexity. Solana development doesn’t have a bunch of L2s (and their investors) lobbying for changes. The primary contributors include L1 client teams (e.g., Agave, Jito, Firedancer), the Solana Foundation, L1 application infrastructure builders, SOL investors, etc.

Overall, I think Ethereum would benefit from more top-down leadership to align everyone. In some ways, Ethereum currently seems to have several of the downsides of a more centralized community without getting the benefits of them.

Solana clearly benefits from a more top-down approach. The ecosystem is more aligned, and they ship faster. It isn’t even the case that the Solana Foundation is out there doing everything or micro-managing everyone. They’re not the greatest operating entity in the world. Importantly though, Anatoly has always very clearly described his opinionated vision for Solana and its purpose. Then, the smaller number of aligned stakeholders go out and execute. The teams close to the metal like Jito are great at executing.

As noted by Prestwich earlier, Vitalik is generally more guarded in expressing his vision for Ethereum. For example, his recent series on “Possible futures of the Ethereum protocol” lays out all of the possible future upgrades to implement and their tradeoffs for us to assess. However, they largely exclude overarching visions. They are relatively un-opinionated about which direction seems like the appropriate strategy at each point and why. They pose questions like “A big question that any L1 scaling roadmap needs to answer is: what is the ultimate vision for what belongs on L1 and what belongs on L2?” without offering an opinion on what the answer is. Let the community look at all the options, and let a thousand flowers bloom.

Now don’t get me wrong, those posts are great. They’re incredibly valuable in helping many people, including myself, better understand the design space to form more educated opinions. However, it’s important to note the marked difference in opinionated stances and visions offered here vs. what other protocol founders do. Anatoly is very clear about his vision for Solana, and Mustafa has clearly defined the core values of the Celestia social layer. This obviously has implications.

Only person who has the moral authority to do so is Vitalik

Doing so requires firing a lot of people explicitly and implicitly (choosing a different cultural value)

Also. His comment is downstream of mine. This is called having a North Star

— Kyle Samani (@KyleSamani) November 7, 2024

The hesitancy to exercise individual power over a decentralized project is understandable, as this can appear more centralized. And yet, as Prestwich noted, “there are still a small number of leaders whose word carries a huge amount of weight.” Vitalik in some ways has a more elevated individual role than anyone in Solana. In practice, most people look at “Vitalik’s roadmap” as the “Ethereum roadmap” regardless of whether they are accompanied by the underlying ideology and opinionated stances. I also notice less willingness in the Ethereum community to openly disagree with Vitalik vs. willingness in the Solana community to openly disagree with Anatoly.

The clearest way for a decentralized ecosystem to align on their high level objectives is for a leader to explicitly set out their vision. Narrative distillation is essential:

“Founders… want their team to have synchronicity around what is most important for the company’s future and how to prioritize and make tradeoffs.

What’s the difference between future investors and potential hires thinking a company is distracted and unfocused versus inevitable and defining? It’s in the coherence of the company’s logic for each sequencing of steps and how legible that narrative is made to them…

Product market fit is just narrative distillation for customers. It only makes sense that this same process is as crucial for investors and employees, too. And just as we have spent so many years reinforcing the primacy of founders focusing on product market fit—and the process of how companies converge on it—so too must founders take distilling their narratives for all audiences equally seriously.”

A north star is an ultimate use-case, like Solana’s “decentralized Nasdaq”.

“A roadmap without a north star is noise before defeat” — Sun Tsu

To me, Ethereum’s north star has always been about the “unstoppable, verifiable world computer” — but I don’t feel it being emphasized… https://t.co/eCBIZGbSIf

— ALEX | ZK ∎ (@gluk64) October 13, 2024

“In peacetime, leaders must maximize and broaden the current opportunity. As a result, peacetime leaders employ techniques to encourage broad-based creativity and contribution across a diverse set of possible objectives. In wartime, by contrast, the company typically has a single bullet in the chamber and must, at all costs, hit the target. The company’s survival in wartime depends upon strict adherence and alignment to the mission.”

– Ben Horowitz, The Hard Thing About Hard Things

Why Ethereum & Bitcoin Upgrade Slowly

This isn’t all just a “centralization vs. decentralization” thing either. A leader can set out a clear vision (the “what”) while many decentralized participants exercise a high degree of autonomy in executing it (the “how”).

Similarly, Bitcoin is more decentralized than Ethereum in most respects. And yet, Bitcoin clearly has a much more cohesive and united vision amongst its community compared to Ethereum’s community. This is downstream of starting with a clear founder-led vision from Satoshi to start.

Obviously Satoshi has since disappeared, allowing the community to chart its own path. When there have been disagreements since then, the Bitcoin community fought it out (e.g., more digital cash vs. more digital gold in the block size wars). This also involved a handful of individual leaders taking more agency in the Bitcoin community to align people at times. Most importantly, the debates reached a clean conclusion. Each side went their own way, and Bitcoin was better for it.

We should reiterate and distinguish between some of the different reasons for why protocols may be slow to evolve.

Bitcoin is mostly slowed down by two of these three:

- Decentralized Leadership – There is no single leader or team to drive change to the extent that other ecosystems have. Changes take years, and coordinating everyone is chaotic. The ability to scale non-custodial BTC ownership is a challenge which needs to be solved. Debates over scaling solutions such as rollups (e.g., Strata) are certainly ongoing. Even in Bitcoin, which can generally afford to be the slowest-moving ecosystem, there is still some real time pressure.

- Conservative – Bitcoin culture is incredibly conservative, and for good reason. This slowness is generally fine (and often even desirable) when your primary goal is to be money. BTC wants to be as predictable and simple as possible. You don’t want to go on vacation for a year then find out the devs changed BTC’s issuance policy.

- Clear North Star – A fragmented North Star is not a problem slowing down Bitcoin today. The endgame is clearly BTC as sound money.

Ethereum is slowed down by all three to some extent:

- Decentralized Leadership – As described above, Ethereum’s leadership and decision making processes have continued to decentralize to a very high degree.

- Conservative – Ethereum has a very conservative culture, stemming from its Bitcoiner roots and the desire of many in the community for ETH to compete as money. This is reflected in the technical and organizational decentralization (e.g., multi-client architecture, ACD) which makes it difficult to ship quickly.

- Unclear North Star – Ethereum has a more fragmented vision. This compounds the difficulty of coordinating across many distinct stakeholders. Many people have conflicting goals, and they argue in circles on important topics for years with little change.

This slow and conservative upgrade pace might be ok if you’re just trying to be money, but it’s a problem if you’re competing as a performant tech platform. If even Bitcoin has some pressure to move a bit faster, Ethereum has a whole lot more need to do so. It has far more credible competition on multiple dimensions, and more of this competition is reliant upon tech differences which require iteration.

What Should Ethereum Do?

Decentralization vs. Performance

It’s unclear to me what exactly Ethereum is optimizing for or why.

step 1: pick an arbitrary spot on the decentralization vs. efficiency tradeoff

step 2: criticize everyone who is more decentralized as not caring about ux

step 3: scramble to make up some reasons why anyone with fewer validators is “basically just running a cefi exchange”

— woodchuck (@txsequencer) September 14, 2024

Many of you probably have “decentralization” or “solo staking” pop into your heads when I say that. On their own though, these are cop-out answers.

Don’t get me wrong, decentralization can be incredibly valuable as a means to very specific ends. For example, decentralized and collaborative operators may provide different levels of censorship resistance (CR). Weaker forms of CR (e.g., eventual inclusion) may provide services to users who would otherwise be excluded from a global financial system. Stronger forms of CR (e.g., FCFS) may be beneficial for specific financial applications. However, these are very different use cases. They require very different types of CR and decentralization. Decentralization is a property, not an end product for users.

Even within decentralization, there is often too little acknowledgement of the fact that these are complex systems with multi-dimensional tradeoffs. For example, Ethereum has actually worsened CR at times in an attempt to preserve validator decentralization (at the expense of builder/relay centralization), when the purpose of validator decentralization is often stated as being to preserve CR.

There are 1 million validators

No followup questions thank you have a nice day

— Jon Charbonneau 🇺🇸 (@jon_charb) June 27, 2024

Due to this lack of clarity, validator node specs remain at relatively arbitrary low levels. Can we increase node’s bandwidth requirements by 25%? 50%? If decentralization is the only goal, then why not decrease the block gas limit, lower the blob count, and increase the slot times? Too often, shouting “aha that’s sacrificing decentralization!” is just used to shut down fruitful debate.

Current state:

Decentralization |-+————–| Practicality https://t.co/nKJJnjJbm2— Dankrad Feist (@dankrad) November 19, 2024

We need to stop arguing over abstract properties and isolated proposals. We need to first decide what the product is. The hard question is asking what is Ethereum uniquely good at doing? The rest will fall out from that. Otherwise, optimizing for arbitrary properties (e.g., vaguely defined “decentralization”, or “neutrality”) without understanding the concrete applications of them is likely to build a very complicated machine that may not be very useful.

The clearest example is the tradeoff between validator requirements vs. performance. Now, this tradeoff should reduce over time as we push the efficient frontier of scaling (e.g., even Solana has ZK-proving the L1 on their roadmap), but that doesn’t change the point here. Concretely, Ethereum and Solana sit at two different places on the tradeoff spectrum today. Solana clearly leans more into higher validator requirements and has higher performance as a result (among many other technical innovations).

To defend a place on the tradeoff spectrum, you need to answer two questions:

1. Do these different (e.g., lower) node requirements result in a different (e.g., more decentralized) validator set?

The shape of the node requirements vs. number of validators tradeoff curve is complicated. Increasing requirements strictly increases the bar for someone to be a validator, thus reducing the possible pool of candidates. However, a more performant chain may be a more useful chain. This increases the utility and value in running a validator, thus helping validator decentralization. Currently, Solana has ~1,400 validators (though notably the Solana Foundation has a delegation program which helps get validators started). Ethereum is in the same ballpark of unique operators (probably a bit closer to the ~6,000 Ethereum nodes currently running).

2. If yes, does this produce tangible benefits?

It’s unclear if either would fare meaningfully differently if major nation states tried to disrupt the functioning of the networks (e.g., requiring validators to censor). In practice, Ethereum validators still have little agency to enforce censorship resistance. This will hopefully change over time (e.g., with FOCIL), but it is not the case today. ~92% of Ethereum blocks are outsourced via MEV-Boost to a very centralized market of relays and builders (two builders currently build ~90% of Ethereum blocks) who can censor arbitrarily. Hopefully new technology such as BuilderNet can improve this market as well.

Kyle described this tradeoff on his recent Bankless podcast:

“It seems like Ethereum’s core value prop is maximal node count which includes at-home solo staking for validation of the L1 chain. That is a value to optimize for. I think if your goal is to win, I think that is the wrong value to optimize for.

These systems are financial systems at their core. From day 1 Anatoly was clear – decentralized NASDAQ, we’re here to build the world’s best, most permissionless, accessible financial market in the world. And a byproduct of that is you could also do payments…

Solana has been very explicitly designed, making decisions architecturally, to try and be the world’s largest global financial exchange, with permissionless access and cryptographically secured asset ownership and all that stuff.

And those are two different value sets. One is like about the validator set. And that may potentially provide certain guarantees. Maybe it’s around censorship resistance… maybe it’s around valid state transitions.

Versus hey lets build the best atomic state machine for financial markets, so that everything just works magically in a single state. And so one is a very user-centric perspective of what do users want, or what do we think they may want. And one is this more abstract notion of CR and state transition validity…

You can argue Ethereum is optimizing for lets say 9 9s of guarantees around state transition validity… You can keep going down the 9s toward the asymptotic failure cases. But there’s also a certain point of ok, but if we’re trading off functionality, and we’re trading off value capture, and we’re trading off ecosystem agility as a whole for the fifth 9 and the sixth 9 and the seventh 9… is that the correct optimization?”

So, how many 9s are actually useful? If you use SOL on Solana or ETH on Ethereum, are you meaningfully more worried that tomorrow the Solana validators might sign off on an invalid state transition compared to the Ethereum validators?

I’m 100% opposed to turning Ethereum into a data center chain. As I’ve said many times, protocols that don’t run on consumer hardware will not be censorship resistant.

But what I am opposed to is using the specter of home staking to oppose any and all changes. The current…

— Doug Colkitt (@0xdoug) June 29, 2024

Ultrasound Money vs. World Computer

I think two (quite good!) talks at the recent Bankless Summit encapsulated the lack of agreement over Ethereum’s core objectives for me:

- Caspar and Ansgar’s talk at Bankless Summit was titled ETH Is Money; If We Choose It To Be. If we choose it to be!

- Justin’s talk noted that Ethereum L1 is competing with Bitcoin, and L2 is competing with Solana. However, the plan to ~100x the L1 execution gas limit and implement “faster-than-Solana” L1 pre-confirmations sounds a lot like the L1 competing with Solana. They both clearly compete today.

I think there are multiple valid directions that Ethereum could go in. Perhaps more importantly than which one, I think we do need to actually pick a direction rather than remain indecisive. This doesn’t mean that Ethereum needs to pick one narrow niche (e.g., just DA). But it does mean that we need to fight out the hard questions and get rid of the ambiguity around fundamental internal conflicts.

What is Ethereum’s unique and defensible moat?

You can make strong arguments for each far side of the spectrum. For example:

Option 1: ETH is Money

ETH as non-sovereign money should be Ethereum’s primary objective.

BTC is fundamentally broken. Having no tail issuance might work for digital cash, but not digital gold. Relying on transaction fees assumes that BTC transactors are the network’s primary users. This makes sense for digital cash. However, BTC has opted to be digital gold. The value of digital gold is primarily to hold it, so BTC holders are the network’s primary users. They should indefinitely pay via issuance for the value they receive. Even if BTC manages to generate meaningful fees over the long-term (e.g., transitioning more from digital gold to digital cash), these fees will be too unstable without inflationary block rewards. ETH is ultrasound money. Even better than BTC’s fixed supply, ETH will be deflationary.

Bitcoin can’t even build real L2s anyway. The BitVM stuff is clunky, and Bitcoin will probably never enable the opcodes needed to bring them on par with Ethereum L2s.

Ethereum watching Bitcoiners build L2s pic.twitter.com/PfIylO6xTc

— Jon Charbonneau 🇺🇸 (@jon_charb) May 29, 2024

ETH can surpass BTC with better economic policy and the necessary technical architecture to scale ETH ownership trustlessly. ETH is permissionless money with strong property rights. Because users all want ETH as sound money, Ethereum is the necessary ledger of record. L2s must come to Ethereum for trustless access to ETH and trustless composability between other chains using ETH. In this world, the slow settlement layer architecture makes sense. Faster and more performant infrastructure (e.g., AggLayer and shared sequencing) can live atop Ethereum, but they must ultimately settle to it.

It’s fine for all execution to leave the L1. Ethereum L2s will be better than Solana anyway. The L1 competing with Solana head-on is a fool’s errand. Solana will always be much faster and cheaper. Ethereum’s regulatory moat (e.g., with an ETF) will soon disappear. Institutions are deploying to Solana as well now. Ethereum would’ve needed to start scaling years ago to compete here. It has too much tech debt, and the culture isn’t to ship fast.